What If Saylor Goes Nuclear: Issuing $20 Billion in Debt for a Massive Bitcoin Play? — What if?

MicroStrategy: The Bitcoin Whisperer of Wall Street

MicroStrategy (MSTR) has evolved into the corporate world’s ultimate Bitcoin evangelist, balancing bold innovation with audacious financial maneuvers. By fusing traditional corporate strategy with digital asset revolution, it’s a fascinating story of ambition, risk, and potential rewards. Here’s a comprehensive look at why this company is making waves and why its proposed $20 billion Bitcoin bond could catapult it into a new financial stratosphere.

2024: A Year of Bitcoin-Driven Growth

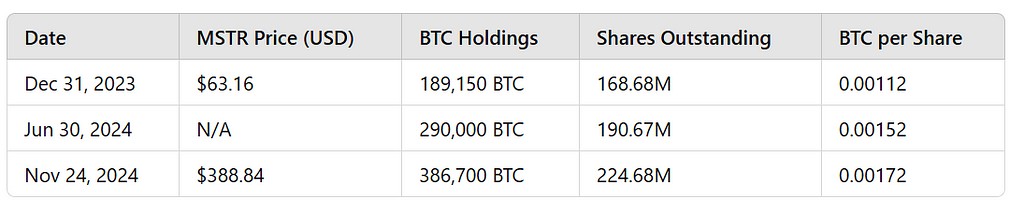

Let’s start with the numbers because, as they say, numbers don’t lie (but they sure can make you sweat):

Translation for mere mortals:

MicroStrategy started the year holding 189,150 Bitcoin (BTC) and ended with 386,700 BTC. That’s almost doubling down on the digital gold. But what’s really fascinating? The BTC per share increased from 0.00112 to 0.00172 BTC, even as the company issued more shares. Yes, they diluted shares and made them more valuable. That’s like diluting whiskey and somehow making it taste better.

The $20 Billion Gambit: Bigger, Bolder, Riskier

IF MicroStrategy now proposes issuing $20 billion in bonds to acquire even more Bitcoin. This is the financial equivalent of throwing gasoline on an already roaring bonfire and inviting everyone to bring marshmallows. Let’s break it down.

What Could They Buy?

At an assumed Bitcoin price of $120,000 (because large-scale buying usually pushes prices up), they could acquire approximately:

Add that to the current 386,700 BTC, and the grand total becomes 553,367 BTC. That’s over 2.6% of all Bitcoin ever to exist. In simpler terms, they’d own a slice of Bitcoin history.

What’s the BTC per Share?

With 224.68 million shares outstanding, the new BTC per share would be:

This represents a 42.7% jump in Bitcoin exposure per share, a win for shareholders who probably didn’t even know what Bitcoin was when they bought the stock.

Stock Price Projections: The Moonshot Scenario

Now comes the fun part: speculation.

If Bitcoin Holds at $120,000

MicroStrategy’s Bitcoin holdings alone would be worth:

Combine this with the market’s multiplier effect (we’ll call it the “Bitcoin Beta Phenomenon”) and an mNAV multiplier of 15, and MSTR’s market cap could soar to nearly $1 trillion. Divide that by the shares outstanding, and you get:

Did you catch that? From $388.84 to $4,450. That’s not just growth; that’s stratospheric.

How This Impacts Bitcoin

MicroStrategy’s purchase of 166,667 BTC would have profound effects:

1. Supply Shock

Bitcoin’s supply is finite. This scale of buying would absorb 0.8% of all Bitcoin, likely triggering a supply squeeze. Prices could rise to $140,000 or more, driven by scarcity and speculative momentum.

2. Institutional Validation

If MicroStrategy’s move succeeds, it could signal to corporations, hedge funds, and even governments that Bitcoin isn’t just an asset — it’s a strategy. The knock-on effects? Massive adoption and broader integration into traditional financial systems.

3. Volatility on Steroids

Yes, Bitcoin’s price will rise, but let’s not forget the short-term volatility circus. Traders will have a field day, and speculators will feast on every price swing.

Inclusion in Major Indices: The Prestige Factor

If MSTR’s market cap crosses $100 billion, it would qualify for elite indices like the S&P 500. Here’s why this matters:

The Upsides

- Institutional Inflows: Index funds and ETFs would be forced to buy MSTR, creating sustained demand.

- Visibility and Credibility: Inclusion signals to the market that MSTR isn’t just a bold bet — it’s a legitimate financial player.

The Risks

- Volatility Concerns: Its high beta to Bitcoin might deter risk-averse funds.

- Regulatory Attention: Any moves that resemble market concentration or manipulation could draw scrutiny.

Risks: Why You Can’t Have a Free Lunch

As bullish as this all sounds, risks lurk beneath the surface:

- Leverage Risks

A $20 billion bond issuance doubles MicroStrategy’s debt, creating financial strain if Bitcoin’s price drops. - Interest Rates

Higher interest rates could increase the cost of debt servicing, eating into profitability. - Regulatory Scrutiny

A purchase of this scale might attract regulatory attention, especially from those who don’t understand Bitcoin’s decentralized ethos.

The Big Picture: A Generational Opportunity

MicroStrategy isn’t just a company; it’s a blueprint for bold corporate strategy in the digital age. By leveraging its balance sheet to accumulate Bitcoin, it has redefined what’s possible in corporate finance.

With an mNAV of 15 and Bitcoin per share poised to rise 42.7%, the potential for exponential growth is tantalizing. Think of MicroStrategy as a high-octane ETF — except without the fees, and with a CEO who seems to genuinely love Bitcoin more than coffee.

In this volatile but exciting era of digital transformation, MicroStrategy isn’t just riding the wave — it’s creating the tsunami.

![]()

What If Saylor Goes Nuclear: Issuing $20 Billion in Debt for a Massive Bitcoin Play? — what If? was originally published in The Capital on Medium, where people are continuing the conversation by highlighting and responding to this story.