In this article we will develop a trading system with a very simple logic, based on the use of the daily range as a measure of market volatility. As will be seen, even an extremely simple and linear rule can give rise to interesting trading ideas, especially when applied to markets characterized by directional moves and phases of volatility expansion such as Bitcoin (BTC).

The idea behind the strategy is to exploit the days when the market shows a certain compression of the move compared to its overall excursion. In particular, the system will compare the body of the bar, that is, the distance between the open and the close, with the total range of the day, defined as the difference between the high and the low. When the body is smaller than a certain fraction of the range, this condition will be interpreted as a possible phase of indecision or compression, from which the market could subsequently generate a more decisive move.

The strategy will then enter long via a stop order placed above the close, more precisely at a distance equal to the range of the bar. In this way, the system will not enter the market immediately, but only if the price actually shows enough bullish momentum to break through the predefined entry level.

The core of the initial code (in PowerLanguage) will therefore be this simple line:

if Body

As you can see, the logic is deliberately essential: the parameter `dFactor`, initially set to 1, determines how small the body of the bar must be compared to the overall range in order to generate a trading signal. To complete the structure of the system, a stop loss, a profit target and a forced exit at the end of the session are then added, so as to keep the strategy on an intraday horizon and avoid overnight exposure.

The session considered conventionally runs from 00:00 GMT to 23:59 GMT, to make it coincide with the calendar day, since cryptocurrencies are traded 24 hours a day. A 1440-minute bar time frame, i.e. 24 hours, will also be used.

In the following paragraphs we will therefore analyze in detail how this logic works, assessing its initial results and possible optimizations of the main trading parameters.

Trading System on Bitcoin: building the initial strategy

Assuming we trade with $100,000 per trade, a hypothetical value to simplify calculations but scalable thanks to the divisibility of the spot market, the trade will be closed when a stop loss of $2,000 is reached (i.e. 2% of the position value). This is a rather wide value but assumed to be necessary in this market, given Bitcoin’s volatility and how nervous its moves can be. In any case, the strategy has an intraday horizon, so it will close positions at the end of the session if necessary, or upon reaching a take profit of $10,000, equal to 10%.

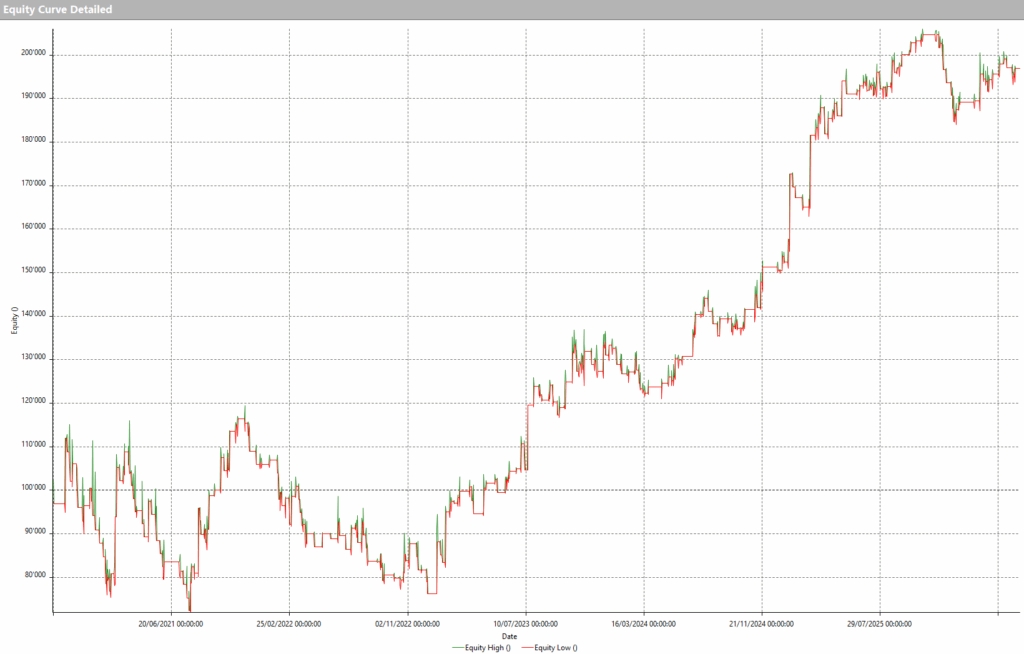

Applying this strategy to the Bitcoin (BTC) spot market against USDT (a stablecoin pegged to the dollar), from January 2017 to May 2026 we obtain very encouraging results, with an equity line that rises in a fairly regular way.

Figure 1 – Equity line of the trading system on Bitcoin (BTC) in the initial configuration

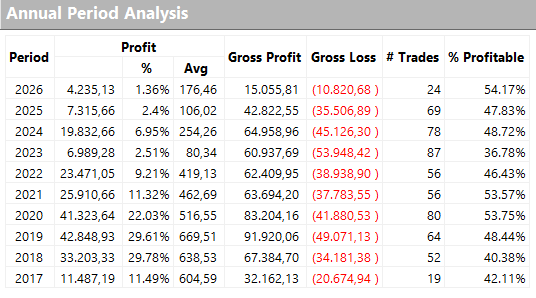

This is confirmed by the annual results shown in Figure 2, which however reveal an average trade that is not very high, especially in recent years, and that could therefore be improved in order to make the strategy more robust with a view to also covering the operating costs of real trading (commissions and slippage in order execution).

Figure 2 – Annual results of the initial version of the Bitcoin trading strategy

Optimization of the Bitcoin trading system: improving robustness and performance

Among the variables that can be adjusted to optimize the strategy there is certainly the multiplicative factor of the range, ‘dFactor’, but also the stop loss and take profit values.

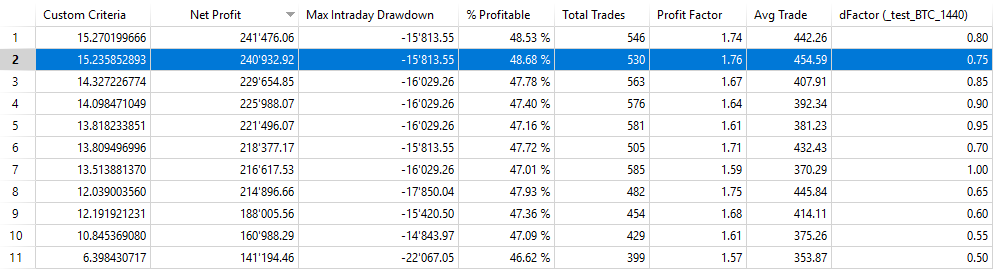

By varying ‘dFactor’ between 0.5 and 1 in steps of 0.05, we obtain the results in Figure 3.

Figure 3 – Optimization of the dFactor parameter of the Bitcoin trading strategy

Sorting them by net profit, we can see that the value 0.75 allows us to obtain an excellent Net profit/Drawdown ratio (the Custom Criteria) and the best average trade (about $454), with the values around it not changing the system metrics very much, confirming the validity of this filter.

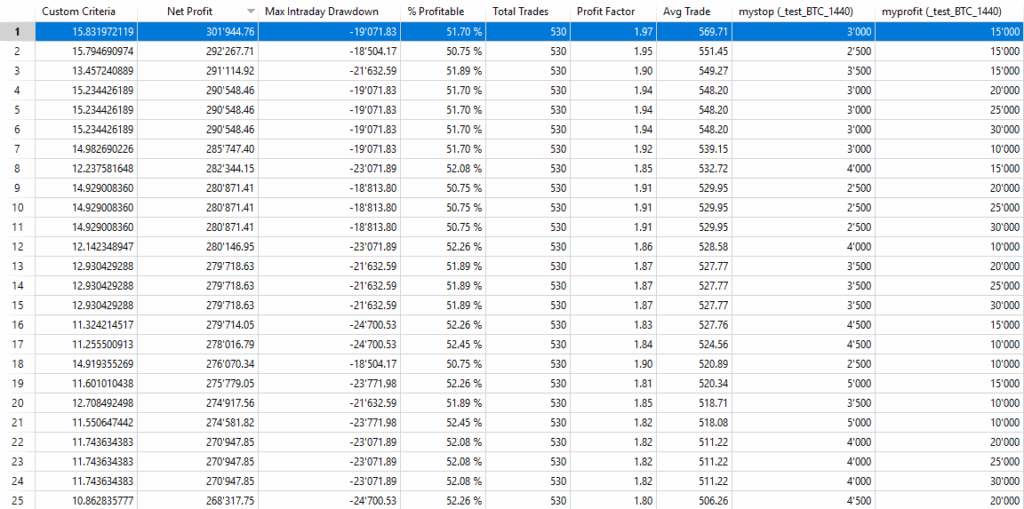

With the selected parameters, therefore, the total profit of the system approaches $241,000 over 530 trades, with an average trade of about $454. These results indicate a strategy that is already quite good and could be applied in live trading, but this does not mean that further work cannot be done to improve it.

At the moment, in fact, the strategy uses a stop loss of $2,000, i.e. 2% of the position value, and a profit target of $10,000. In Figure 4 we can see that by varying the stop loss from $1,000 to $5,000 and the profit target from $0 to $30,000, the pair of values $3,000 and $15,000 turns out to be optimal in terms of the Net profit/Drawdown ratio.

Figure 4 – Optimization of stop loss and take profit of the Bitcoin trading strategy

Validation of the strategy on other cryptocurrencies: Ethereum, BNB and Solana

Without going further by adding trading filters that could easily lead to overfitting in the optimization of the strategy, we could simply try to validate it by applying the same logic to other cryptocurrencies, to check whether it can also achieve good results on them. It is well known that Bitcoin somewhat leads the entire market, so the other cryptocurrencies tend to move in a similar way.

Below are the equity lines of the same strategy applied, with the same parameters, to Ethereum (ETH), BNB and Solana (SOL), three of the main altcoins in the crypto market.

Figure 5 – Equity line of the strategy applied to Ethereum (ETH)

Figure 6 – Equity line of the strategy applied to BNB

Figure 7 – Equity line of the strategy applied to Solana (SOL)

The upward trend of all the equity lines confirms the soundness of the strategy, although to obtain the best results for each of the cryptocurrencies considered it would be advisable to optimize the parameters, as was done previously for BTC. This work is therefore left to the reader as a trading exercise.

Conclusions: can a simple trading system on Bitcoin work?

In this study we developed an extremely simple trading system on Bitcoin, based exclusively on the behavior of the daily range and on market volatility.

The results show how even essential trading logics can offer interesting ideas when applied to instruments characterized by strong directionality and wide moves such as Bitcoin (BTC).

The subsequent validation on Ethereum, BNB and Solana also suggests that the trading principle behind the strategy may be present more generally in the cryptocurrency market.

Of course, no strategy is a universal solution and every approach requires thorough testing, risk control and continuous validation. However, this example once again shows how simplicity, robustness and method can often represent an effective combination in the development of trading systems on crypto markets.

Until next time, and good trading!

Andrea Unger