Vitalik Buterin is challenging one of DeFi’s most familiar safety mechanisms: the automatic liquidation that closes a debt-backed position when collateral falls below the required backing for the loan.

In a June 1 Ethereum Research post, Buterin proposed building synthetic, index-tracking assets on top of options, with collateralized debt removed from the base design.

The idea would remove the hard liquidation trigger from the base design and replace it with a slower form of risk: the user’s exposure drifts away from the target unless the position is rebalanced.

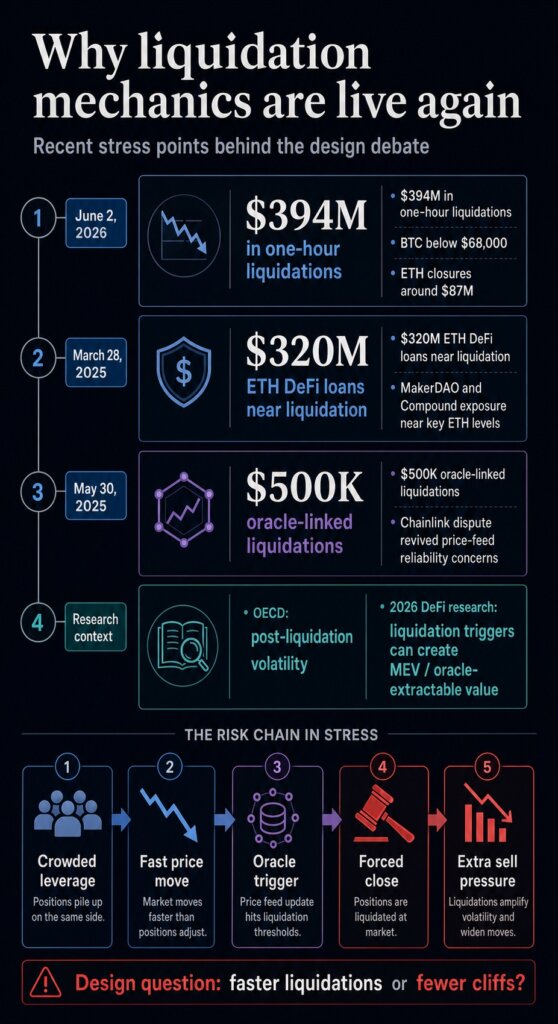

That distinction is important because the old mechanism is still showing up in market stress. Bitcoin‘s fall below $68,000 triggered about $394 million in one-hour liquidations on June 2, including roughly $87 million in ETH positions, as leveraged bets were force-closed across the market.

The flash crash came one day after Buterin’s post and serves as a market reminder: when price moves hit crowded leverage, automatic closures can turn a drop into a wider market event.

The proposal is research-stage architecture: a design argument separate from any protocol launch, Ethereum roadmap commitment, or direct replacement for Aave, Maker, or existing stablecoins. It shifts the focus from collateral buffers and faster price feeds to a more fundamental design choice: whether instant liquidation should remain DeFi’s central means of surviving a crash.

Why the safety switch can amplify stress

Most DeFi lending systems are built around the same basic problem. A user locks in collateral, borrows against it, and must keep the position above a required safety level.

In Aave’s borrowing documentation, that level is expressed through a health factor. When it falls below 1, the position can be liquidated: a liquidator repays debt on the borrower’s behalf and receives collateral plus a bonus.

That structure protects the protocol’s solvency, but it also concentrates action at the worst possible moment. If ETH or another collateral asset falls fast enough, users do not choose when to sell. The system chooses for them.

Liquidators compete to close eligible positions, and the collateral can be pushed into markets already short on liquidity.

The record supports that concern. An OECD working paper on DeFi liquidations found a positive relationship between liquidation activity and post-liquidation price volatility across major decentralized exchange pools.

The paper also emphasized that liquidators rely on available liquidity during stress, which means the mechanism designed to restore balance can run into the same liquidity shortage as everyone else.

CryptoSlate has previously covered the operational version of that risk. A 2025 Chainlink-related oracle dispute led to more than $500,000 in liquidations on Euler Finance and revived questions about how protocols should interpret pricing data in illiquid markets.

Separately, a 2025 ETH decline put nearly $320 million in Ethereum-based DeFi loans within 20% of liquidation, with MakerDAO and Compound exposure concentrated near key price levels.

The common thread is the cliff. DeFi needs a way to handle undercollateralized positions, but the current method often waits until a number is breached and then requires immediate action.

That creates a crowded moment for borrowers, liquidators, oracle feeds, and liquidity providers simultaneously. It also gives sophisticated actors a clear trigger to watch, because the protocol rule announces when a position becomes profitable to close.

For users, the practical consequence is straightforward. A liquidation system can protect a lending pool while still giving the individual borrower the worst possible execution window.

The user may have intended to keep long-term ETH exposure, hedge a cash need, or wait out a sharp wick. Once the threshold is crossed, the system’s priority becomes solvency, and the user’s timing preference disappears.

How options turn a cliff into drift

Buterin’s alternative starts by changing the primitive. A position that can become undercollateralized gives way to a split ETH claim: the proposal divides 1 ETH into two option-like assets, called P and N, tied to a price index, strike price, and maturity date.

At maturity, an oracle resolves the index value and determines how much of the ETH claim each side receives.

The key property is simple: P and N always add back up to 1 ETH. Because the system is dividing a fixed ETH claim between two sides, it can avoid seizing collateral from a borrower to close a deficit.

In Buterin’s framing, the design removes the liquidation event by construction.

For a user trying to hold synthetic dollar exposure, the practical experience differs from a debt-backed stablecoin. In the debt model, a user can appear fully hedged until the collateral threshold is breached, at which point the position is force-closed.

In the options model, the holder avoids the sudden close, but the position can gradually stop behaving as the user intended.

Buterin’s example uses a user who wants some level of dollar exposure while ETH is trading around $2,500. The user could buy a deep option tied to a lower strike, such as $1,500, and rotate into lower-strike options if ETH falls toward the original strike.

If the user does not rebalance, the exposure drifts. The user keeps a claim, but the hedge becomes less exact.

That is the central tradeoff. The design keeps risk in the system, and changes who controls the timing and what form the damage takes.

Liquidation-based systems outsource the decision to a protocol rule and liquidator bots. The options-based design pushes more of that decision toward users, wrappers, market makers, or automated rebalancing systems.

Buterin also acknowledged a limit for stablecoin use. A medium amount of annualized drift may be acceptable for someone seeking price stability relative to future expenses.

It is much less useful for an accounting stablecoin, where users want to treat the token as a dollar for payments, bookkeeping, or tax reporting.

The oracle tradeoff

The oracle argument may be the proposal’s most important protocol-design claim.

Debt-backed liquidations depend on real-time price feeds. A protocol needs a binding price quickly enough to determine when a position is unsafe and to allow liquidators to act.

Buterin argues that this constraint makes real-time oracles hard to secure because they rely on automated actors watching live signals and leave little room for slower dispute resolution.

Options move the critical oracle call to maturity. Oracle risk remains, but the time pressure changes.

If a system can wait to resolve a contract, it can use slower, more contestable mechanisms, including prediction-market-style approaches or expensive fallback oracles that would be impractical for instant liquidation.

That is why the proposal is more than a stablecoin tweak. It shifts DeFi’s risk architecture away from a single live price that can trigger irreversible action.

Recent research on liquidation dynamics in DeFi shows why that surface is central: liquidation mechanics can create incentives around price manipulation, MEV, and oracle-extractable value when a profitable closure depends on a market price crossing a trigger.

The benefit still depends on implementation. A wrapper that automatically rebalances for users could make the product easier to hold, but it could also recreate visible timing rules that sophisticated traders can anticipate.

A purely local user agent could hide some timing choices, but would raise its own usability and execution questions. An onchain DAO wrapper would need deterministic rules and deep markets to avoid becoming another predictable target.

Slow oracles help only if the rest of the design avoids forcing the same problem elsewhere. That is the tension Buterin’s post leaves for builders.

A slower oracle can give a system more time to settle disputed information, but users still need markets deep enough to rotate exposure and rules strong enough to avoid turning every rebalance into an exploitable signal.

The comparison with prior oracle disputes is useful here because the risk arises when bad data meets a rule that must act immediately.

The options design reduces the need for that instant decision, while builders still have to decide who watches the index, who provides liquidity, and who absorbs losses when the market moves faster than the hedge.

What developers still have to prove

The next test is whether the market structure around Buterin’s idea can be competitive with the debt systems it would challenge.

The proposal itself flags slippage as a major risk. Rebalancing through ordinary automated market makers could be expensive, especially if users need to rotate option exposure repeatedly during volatile periods.

Buterin suggested that rebalancing might need a different market structure, closer to patient one-sided market making than an instant sell.

That requirement is the adoption test. If users avoid liquidation but bleed too much value through drift, slippage, or operational complexity, the model becomes elegant research rather than useful DeFi infrastructure.

If builders can make rebalancing cheap and less exposed to attack, the idea could become a serious alternative for users who want price stability without signing up for a liquidation cliff.

The same test applies to stablecoin framing. The proposal is most defensible when described as a way to hold a stability-oriented exposure or personal hedge.

It becomes weaker if marketed as a simple dollar replacement. A token that drifts away from its target and needs periodic rotation is a different user promise from a redeemable dollar, an overcollateralized stablecoin, or a conventional CDP-backed synthetic.

For Ethereum, the significance is that one of its most influential designers is treating liquidation as an architectural choice rather than an unavoidable fact of DeFi.

The next signal is whether any protocol team turns the options model into a tested wrapper, simulation, or live market with sufficient liquidity to demonstrate the trade-off in practice.

Until then, the proposal is best read as a direct challenge to DeFi’s crash mechanics: the industry can keep trying to make liquidations faster and better collateralized, or it can test designs built without sudden forced sales.