Circle’s IPO on June 5 garnered significant attention, representing a major moment for stablecoins and the wider cryptocurrency ecosystem. As the total stablecoin market capitalisation recently surpassed $250 billion, continuing its sharp upward trajectory, the financial world is increasingly waking up to the profound shift that’s taking place.

Yet, while most coverage has focused on valuation speculation, listing mechanics, or how it compares to Coinbase, there’s more to this than meets the eye. Rather than just being an isolated liquidity event or fintech story, Circle’s move to the public markets is much more of a turning point in how digital financial infrastructure is being perceived, valued, and integrated into the broader economy.

Circle and the coming IPO wave

On May 20, Circle confidentially filed to go public, its second attempt following a terminated SPAC deal in 2022. Timing matters here. This is not 2021, when crypto IPOs were more about retail FOMO and bull market froth, and the 2025 version comes amid a very different set of conditions: US spot Bitcoin ETFs have been approved, trading volumes are recovering, stablecoin legislation is actively moving through Congress, and institutional capital is returning in a more use-case-driven, long-only fashion.

The IPO itself was nothing short of remarkable. Priced at $31 per share on June 5, 2025, Circle’s stock surged 168% on its debut day to close at $83.23, with a further 30% jump to $107.70 by June 6, reflecting a nearly 250% two-day gain, the highest since 1980 according to Jay Ritter. This explosive start pushed its market cap from an initial $6.8 billion to over $21.6 billion, though it left approximately $3 billion on the table due to underpricing, a common Wall Street strategy to ignite investor enthusiasm.

The market’s reception of Circle will likely set the tone for a string of other digital asset infrastructure firms considering public listings. Companies like Paxos, BitGo, and even Thiel-backed players with stablecoin exposure have been quietly preparing to enter public markets. Here, though Circle’s IPO gives them a blueprint and potentially a valuation benchmark, it is the broader legitimization of ‘stablecoins as infrastructure’ that is more of a meaningful shift than many are currently pricing in.

Stablecoins: the rails, the oil, the distribution layer

To really understand why this IPO matters, it’s important to look beyond the token (USDC) and focus on the underlying model. Circle earns yield on reserve assets, typically short-term Treasuries, that back the USDC supply 1:1. This is a business is essentially built on capital efficiency and regulatory compliance, not speculative tokenomics, and it’s now becoming a platform for much more.

Circle’s strategy is increasingly about positioning USDC as a settlement layer for the internet. That includes merchant payments, treasury operations, cross-border flows, and the eventual integration of real-world asset (RWA) tokenization. But here’s where it gets interesting: most stablecoin activity today still revolves around trading and investing, not payments, remittances, or RWAs.

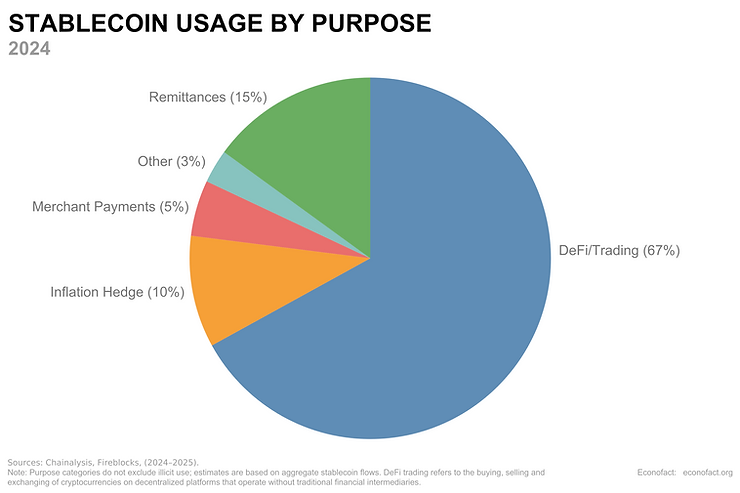

As per the chart above, approximately of 67% of stablecoin velocity is still driven by capital markets activity: funding crypto trades, moving funds across exchanges, and arbitrage between ecosystems. That’s a clear sign we’re still in the early monetisation phase of the “picks and shovels” layer as the future utility of stablecoins’ liquidity, portability, and programmability will only rise as more and more of our lives, infrastructure, and financial ecosystems go digital.

The GENIUS Act: policy clarity meets public markets

The timing of Circle’s IPO also intersects with meaningful movement on the policy front. The GENIUS Act, the first federal framework for stablecoins, passed the Senate on June 17 with rare bipartisan support (68–30), granting sweeping oversight to the Treasury and opening the door for banks, fintechs, and retailers to issue dollar-pegged tokens.

While most headlines focused on regulatory clarity and US dollar strength, the broader implications are quietly profound. The Act accelerates the US dollar’s export via private stablecoins, potentially making tokenised Treasuries held by firms like Circle more trusted than some local central banks.

It could also give new momentum to “bridge assets” like XRP, which stand to benefit from fragmented stablecoin ecosystems that require cross-network settlement. Ethereum, which is still the core infrastructure for stablecoins and DeFi, may also be an indirect winner as it becomes further entrenched as the operational backbone of digital finance.

The Act still needs to be reconciled with the STABLE Act in the House, but for now, it marks a historic shift in regulatory acceptance catching up with market adoption.

Lessons from early adopters like Tron

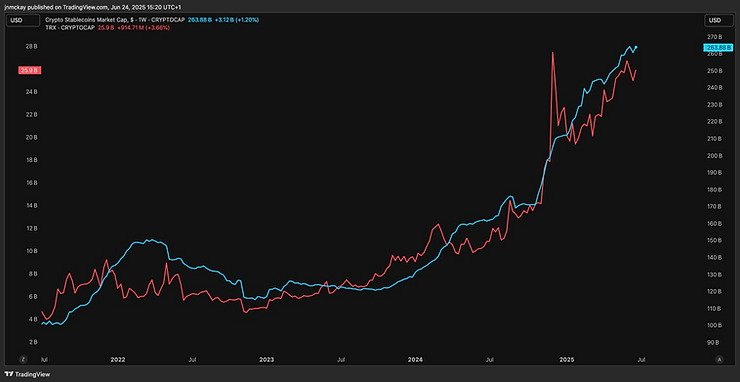

To understand where stablecoins are headed, it helps to look at where they’ve already thrived. Tron’s ascent to the 8th spot in global crypto rankings and now with a market cap of over $26 billion, offers a blueprint for this shift. As the largest settlement layer for stablecoins, Tron processes 2,000 transactions per second at near-zero fees (often less than a cent compared to Ethereum’s $10+) handling 8.5 million daily transactions with 99.7% block reliability. The network’s $694.5 billion monthly USDT transactions, driven by Tether’s 90% dominance in stablecoin payments, reflect its utility focus.

The chart above spans 2022 to 2025 and shows Tron’s growth mirroring the total stablecoin market cap, breaking into the top 10 in Q4 2024. With 6 million daily active addresses rivaling Solana’s relative scale, Tron’s success stems from early stablecoin adoption. Investors are starting to notice, but few connect this to the infrastructure potential Circle’s IPO heralds.

One of the key data points here: the top 10 wallet clusters on Tron are highly cyclical, suggesting that stablecoins are being used for short-term working capital rather than passive storage. This supports the thesis that stablecoins are less like savings accounts and more like transaction fuel meaning that they function as infrastructure, not end-state assets. Ultimately, the chains that win stablecoin flows tend to win users, developers, and ultimately, enterprise adoption.

Conclusion: flagship IPO, new trajectory for digital finance

In many ways, Circle’s IPO is less about what stablecoins are today, and more about what they’re about to enable across the domains of tokenized treasuries, RWA marketplaces on public blockchains, settlement infrastructure for cross border payments or private banking networks, and more.

At the same time, the IPO isn’t just about access to capital, but exposure to scrutiny, regulation, and institutional alignment. This may well prove to be an asset in itself, especially as investors begin distinguishing between digital assets projects that operate like protocols and those that operate like financial service providers.

The market often underprices infrastructure because it looks boring. But when infrastructure is what the next financial stack is being built on, it becomes anything but.

For more information about our custom research services please get in touch directly, contact us here, or subscribe at www.mckayresearch.com/analysis to get our latest analysis on digital assets trends.

![]()

Beyond the IPO: What Circle’s Listing Means for Stablecoin Adoption was originally published in The Capital on Medium, where people are continuing the conversation by highlighting and responding to this story.