Before we begin: There are two forms to this Financial Market Outlook for 2024. The one published through Medium and Substack is the concise version around 4000 words.

Whilst the full in-depth report is available to purchase in PDF format on our website for £8. This is around 7000 words and includes a separate PDF of our Investment & Quantitative Analysis Report which is a framework that is tracked and proven with past market data to be very effective when investing. The full version also includes sections such as in-depth on inflation, the debt situation as well as the bullish thesis for 2024. If you would rather this version it is £8 on our website. (labyrinthcapital.co.uk)

Introduction:

The final FOMC meeting of 2023 has set the stage for an intriguing economic landscape in 2024. With indications of three interest rate cuts in the upcoming year, the market has taken a bold stance by pricing in a more aggressive scenario, anticipating a 1.5% cut — twice as much as the Federal Reserve’s expectations. In this report, we will be covering the 2023 recession that wasn’t. After many economists and speculators called for a market downturn, the year turned out to instead incur impressive economic growth with markets skyrocketing close to all-time highs. How did this happen in a high-interest rate environment with quantitative tightening in full motion? In one word? Liquidity. We will be exploring why the recession didn’t manifest and conduct a thorough approach for you to utilise as we set up for the new year.

Fiscal situation:

So why was the economy more robust than most people thought? There were a number of reasons but a large one is that fiscal spending in the US was so strong. What many ignored was that there was huge fiscal expansion which lifted the economy. This encouraged a positive wealth effect to brace the consumer. Fiscally the US had near-record deficit spending in 2023, and many say they’re doing it because of the election.

The fiscal situation was underestimated by investors. We have been heavily reliant on private credit for a significant period of time. It got to the point where we eventually stacked so much private sector debt that we hit the GFC. Then in 2008, the FED tried to fix everything with monetary stimulus, lowering rates to 0% which did not work. They then tried QE2. QE3. This didn’t work either. Then you fast forward to COVID. The Central Banks had known that monetary stimulus didn’t work, so they explored and had prepared, other ways to create money. The lowering of rates served as a tool to encourage banks to lend, enhancing private credit creation and they spent this money into existence (as we saw through the bull market with valuations). The FED focused largely on fiscal, performing way too much. When you look at fiscal as a % of GDP, America came out of the pandemic at almost 25% of GDP. So not only did we have monetary stimulus, but an unprecedented, never done before, shift where the government put money straight into people’s pockets (helicopter money) and a shredding of supply lines.

Again, I will reiterate. Most investors got caught with their pants down because we have continually underestimated the power of the COVID fiscal. To the point where even with depleted savings, or high credit card balances, there is still a lot of liquidity washing around the system. There are even bills like the Inflation Reduction Act which have not even been properly implemented yet, they are simply seeping through.

So, the ones (us included) who thought tightening would stop the economy have been greatly mistaken as we underestimated the power of fiscal alone. It’s almost like this, the banks and FED are pulling on the monetary breaks whilst the government and fiscal side is comfortably winning with its bills on the other. If we think about it, these bills alone are designed by the ‘governments’ to haul manufacturing back to the states too, which is a large reason why we have barely felt the job losses through NFP. So, how long can this fiscal winning out over monetary efforts occur? Well, it is likely that we see a continued rise in 2024 as the ‘party’s’ spending is based on the election cycle. However, just because the economy is doing well, this won’t mean the stock market is going to reflect this.

The notion that the markets are currently following is the Modern Monetary Theory. This theory perpetuates that deficits are not always harmful and can be used strategically to address economic issues. MMT proponents believe that a focus on full employment and price stability is more crucial than an obsession with balancing the budget. Now, this alone sounds ridiculous, that governments can spend money into existence until real resources are constrained, and then from then on we get inflation. However, it is becoming increasingly normalised by the actions of policymakers. As we have consistently talked about the ballooning debt and how the powers tend to not care about the debt until CBDCs come into play, it is very likely that we are simply in a new era where we have continued fiscal spending and it will go up and down in waves, in cyclical moves where we will use fiscal to fix recessions. If this is the case which I am beginning to believe, then portfolios must be adjusted according to this theory alone. With this, it is likely that we have higher sets of inflation for some time to come and that eventually, the actual ceiling for inflation will flip the FEDs made up 2%, and become the floor.

Rate cuts are coming:

So we have established a large cause for market upturn in 2023, but what can we expect for 2024? Well, something we can almost certainly anticipate is the incoming rate cuts by the FED. At the last FOMC meeting, Powell gave a clear signal to the markets that rate cuts were on the horizon.

Contrary to the popular narrative from mainstream educators that rate cuts bring about a utopia of meme stocks and increased liquidity, the reality is quite different. In fact, Labyrinth Capital is putting itself out there in that the incoming cuts will be a short-lived utopia for the markets, resulting in only slightly cheaper debt amid continued tightening measures. We believe this as long as the FED continues rolling over their balance sheet of course.

What the market is currently doing is overpricing optimism into asset pairs, fuelling tech stocks, crypto, and speculative assets. The 10-year yield alone has been dropping below 4%, reflecting the broad expectation of lower borrowing costs. To note, Powell emphasized during his presser that inflation has significantly come down but outlined the central bank’s renewed focus on dialing back. The acknowledgment of decreasing inflationary pressures aligns with the broader economic goal of maintaining stability and ensuring long-term growth and the market took this news almost too well. Once again, a crucial aspect discussed during the meeting was the Federal Reserve’s commitment to QT, the component we have raved about a lot over the past year. This strategy initiated in May 2022 involves the reduction of the central bank’s balance sheet by allowing its assets, mainly consisting of treasuries and mortgage-backed securities (MBS), to roll off. This approach is of course, in stark contrast to QE, where the central bank injects cash into the financial system by purchasing assets.

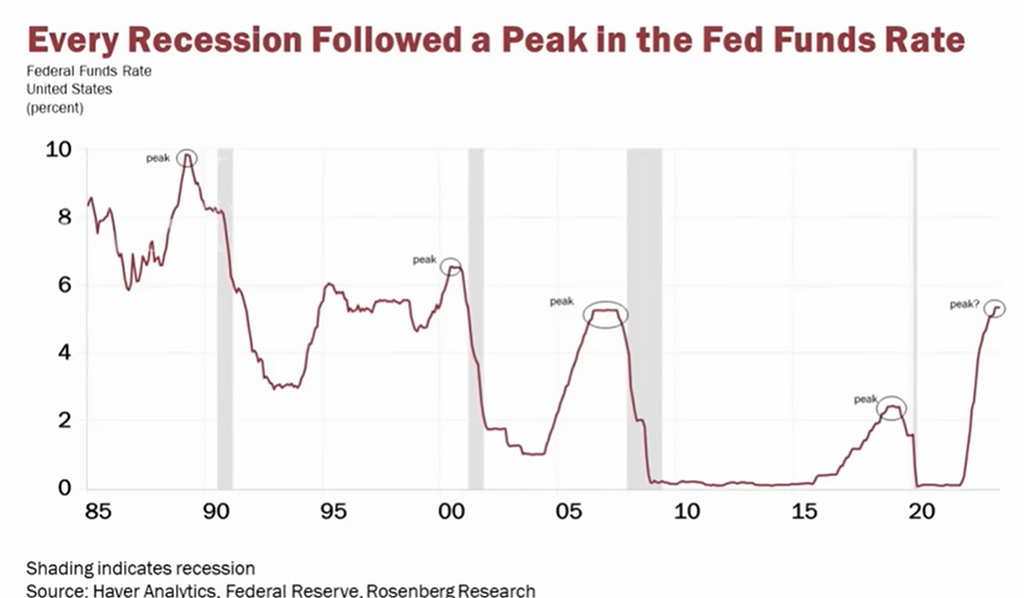

A chart we have posted consistently is the one below, showing that there have only been two times in the past when every time rates were cut, it occurred during or right before a recession began. The last time it happened was 2019. The truth is that even with interest rate cuts, they themselves will take time to actually start being felt in the economy, much like the lags, which means it will take till 2025 to feel the effects. But as always, the market will attempt to front-run this.

Further points we can certainly assume is that the FED is now looking to pivot after peaking in interest rates. This means we shouldn’t expect higher rates anytime soon. Looking back we can see that as we got closer to the target, the FED reduced the pace of tightening. They were essentially trying to find a sufficiently restrictive level. So, on September 20th, the market thought Powell would stop tightening and got caught off guard by the hawkish stance. This resulted in the 10Y rising above 5.5%. The pain the markets felt was a huge correction and tightening of financial conditions from September 20th to the end of October. Following this, the FED clearly felt they hit a suitable level of pain. This was the first pivot. Once again, this came as a surprise whilst they were tightening and the large move down in yields was a result of the initial pivot. As conditions loosened, we got to the point where we surpassed the point prior to where the market was worried in September. Around this level, is where most people believed the FED would turn hawkish once again or calm the market or at least push back on the easing but that is not what happened. This caught many people and spurred speculation further.

So why was this exactly? Well, it is clear that the FED faces a compelling rationale to lower rates and steepen the yield curve. It is my belief that something spooked them. While fiscal policies may provide optimism about the current economic cycle, the long-term trend deeply relies on private sector dynamics as we have discussed. Institution-grade trade is required. Therefore, the role of regional banks is essential in supporting productivity. Regional banks are the ones which were on the brink of collapse. If the stock market declines or we face some systemic economic turmoil, it’s likely that the FED will stop QT and switch to severe cuts, remember they are always reactive, in which case, we should not be surprised. Furthermore, the spectre of hitting critical debt levels before 2050 is also looming large.

Furthermore, the portrayal that inflation is sticky is no different from “inflation is transitory”. The difference now is that the economy is actually reacting, one may say, in order. The bounce and consolidation around 3% in CPI is equally no surprise. What investors must work out is, if the comments about continued QT whilst cutting rates are the FED playing bluff. The FOMC has consistently stated they do not see a recession either.

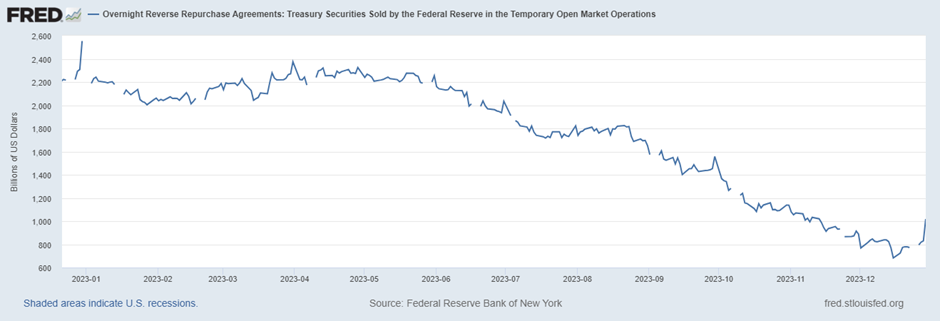

Reverse Repo:

Whilst Powell has reiterated that despite the discussion of interest rate cuts by the committee, there are no plans to halt QT. It seemed that this decision was broadly based on the anticipation for the Reverse Repo Facility to go to 0 and remain there. The Reverse Repo Facility is what we have been hammering on about for the last months in various articles. It has always been there as a source of liquidity for the system to feed off and will be depleted soon, which in essence, will not be net helping the markets and therefore, the tightening (if carried on) will be felt more.

Powell also highlighted the current reserves of banks, standing at $3.27 trillion dollars, emphasising that QT will persist even with rate cuts on the horizon. For context, the correlation between QT and the decline in bank reserves is that with QT continuing, there is an inevitable bleed into bank reserves, signalling a potential shift in the dynamics of financial institutions. Once again, if we are to take Powells’ word (which does not stand on much), the situation looks bleak however, logically adds up.

The likelihood is that when the reverse repo hits 0, around the March—May period, bank reserves will be affected, reaching a dangerous point, likely where Powell then decides to halt QT. This is a large reason as to why we are currently long equities. The liquidity is there to be flushed into the market through money markets, and up until the reserve is drained, it is likely this uptrend can continue. Labyrinth Capital has always maintained that the reverse repo facility is a key source of liquidity and has seen a decline in other deposits of commercial banks’ liabilities. Powell’s commitment to this path suggests and backs our thesis that a mere 25 basis points rate cut may not provide the expected relief, especially as companies refinance at rates almost twice the refinancing rate.

Once again, the estimate is to be depleted in a matter of months which coincides with when the market anticipates rate cuts to begin which is no coincidence of course.

The reality is that the fiscal stimulation and perception of liquidity pushed the market in 2023 and will continue to likely do so in 2024. What people perceive as liquidity which is the fiscal bills and depletion of RRP is the dynamic that pushed a huge end-of-year rally in stocks.

Lag Effect:

Another topic that will need to materialise in 2024 is the lag effect of rising interest rates. This is still a heavy and backed-up case for bears. The tighter monetary conditions, the higher cost of capital, and rising lending standards are historically known to directly increase the gravitational pulling down on economic growth up until something breaks. The narrative the market is currently driving is that this time is different.

One thing we should acknowledge is that it is likely that we inflected early, as Winter was a positive period for the market. The biggest bond rally since 1980 pulled forward a large part of the gains in November as well as the market essentially reading the pause and now cuts as news we are moving back to 0% rates and the money printer.

Again, QT has not stopped, so the lag effect based on the current tightening playing out will theoretically ease into the market around 2025. As we move further into 2024, we will likely see our first-rate cuts, but as we have talked about already, it’s anticipated that the efforts are to be thwarted by lag effects continuing to push the economy from whatever marginal effort of tightening was in the vase of QT. Again, this intrinsic approach will reflect largely on how Powell presents himself at upcoming meetings as well as watching the bond market and where we are likely to draw to.

Furthermore, a lot of the debt is to be refinanced in 2024. As corporations refinance at higher rates, it will be at levels more than twice what they currently have on the books. These businesses have been sitting on cheap debt hoping that Powell will cut so that by the time they re-finance, the rate will be low again. But if not, this hit will go to profit and losses, and expenses will have to be shed which is where we expect potential layoffs to come into play.

The job market is the one factor keeping the outlooks more sustainable than imagined. After all, with recessions, you need higher unemployment, which has not occurred. The unemployment rate has not shot high enough for investors to worry. Essentially, as this debt maturity wall comes to fruition, we should expect higher unemployment around Q2.

The lag effects since the FED actions take time to manifest and eventually pull economic growth down slowly. The problem with the lag effect is the lag. Do we really think the economy is growing at 5%? It is therefore likely, that we experience a correction and I think the largest sign of this will be if job layoffs increase and unemployment rises.

Precious Metals:

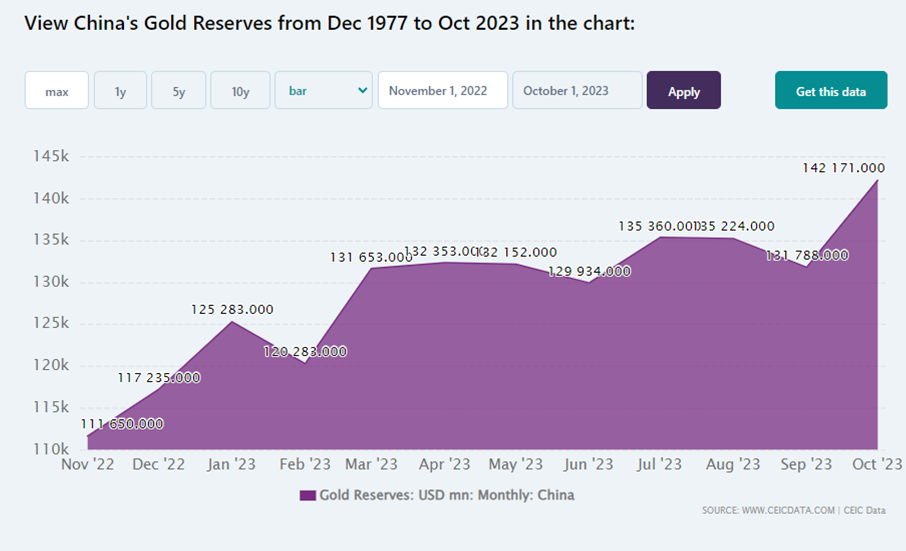

For 2024, we are bullish on commodities. This is for a variety of reasons which we will list. Generally, we have talked a lot about our adoration for commodities like Gold and Silver, but this is likely to be amplified this year as the environment looks more indecisive than ever. One event that has negatively affected the US, was when Russia invaded Ukraine. What this did was send a message to the world that America was fine with openly weaponising the financial system with confiscation of FX reserves. When you look at countries like China and the BRICS nations, this obviously puts them on edge. By no means am I calling for de-dollarization, but we believe that there will be significant geopolitical events that will positively affect commodities.

Simply, if we look at the percentage of dollar reserves China holds in comparison with gold it is a miniscule amount. So if China were to move its reserves to the same level other countries are currently at, it would require tons of gold buys and we see this as a likely output.

If we look at the past year, we had rising interest rates with the dollar rising for a large part, and at the same time, gold hit all-time highs. Now traditionally, higher interest rates have been a kryptonite for gold. Therefore, we can largely assume manipulation and mass buying by Central Banks to fill gold reserves. Equally, this coincides with the burgeoning debt issue too. Ultimately, the market showed us that you don’t need increased inflation for gold to function to its purpose because, at its core, it is a monetary inflation hedge. So when the dollar goes down and interest rates get cut, this will add the extra push to gold to seek standard deviations. All in all, precious metals are a safe and logical bet for not just 2024, but beyond that and we will be buying at whatever price.

Our targets for Gold are the following:

H:$2170

L:$1800

Equities:

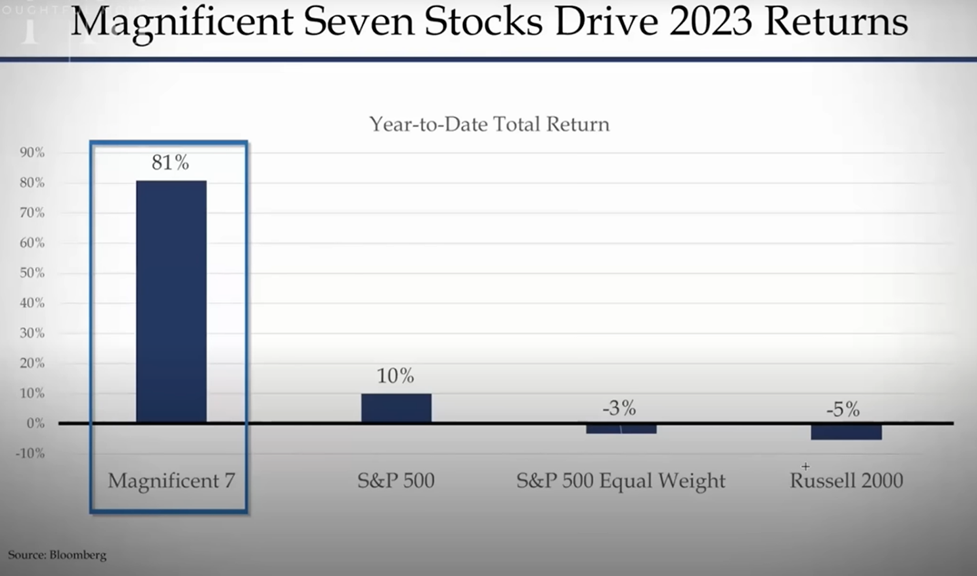

The rally in equities leading from the October period was extremely unexpected as mentioned in prior sections. As well as the reasons mentioned, the FED was also deeply expanding its balance sheet. Furthermore, the markets were spurred on by the AI frenzy. The AI plays were largely the Mag 7 stocks too which YTD contributed to over 100% of SPX’s growth. This is insane when you compare SPX’s growth minus the Mag 7 which is around 10%.

As we move into 2024, investors are confident in the mag7, believing we are entering a prosperous environment where the economy will keep them inflated. The problem we have with this stance is that everyone is piling into these stocks. They have borrowed long and been bought so hard that everything else is cheap, small caps, etc. This also goes for foreign assets too. This has largely changed since Powells’ pivot as they’ve run up recently but there was clear and significant crowding in those names. We believe that there will continue to be opportunities in small caps, crypto, and foreign stocks.

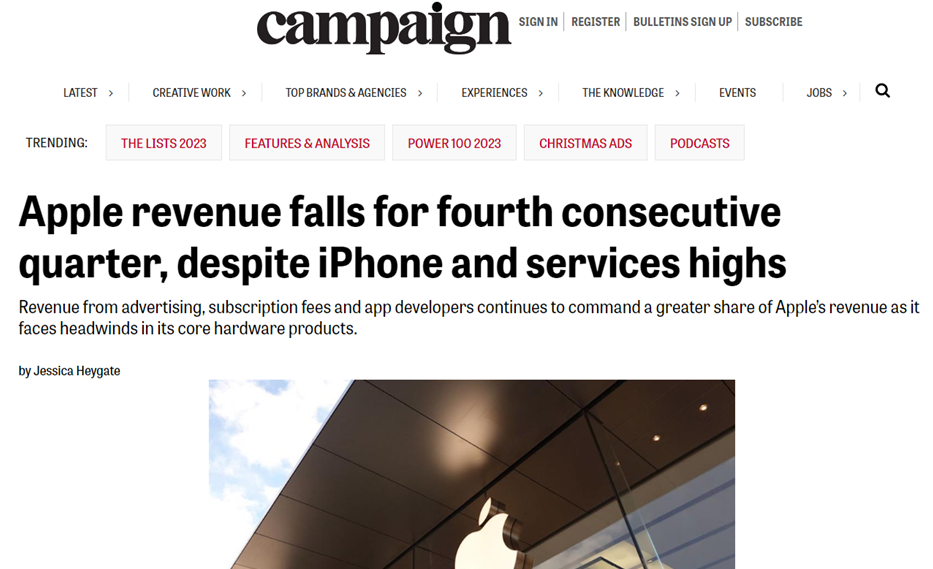

We are currently at the point where companies are experiencing negative sales growth e.g.: Apple has been one of the Mag 7 that are enjoying positive PEs, and get the majority of dollars in the market through passive ETF indexing, but are having negative sales over consecutive quarters. It really is a market of pure speculation.

Again, the bull case for the upcoming year is closely tied to liquidity trends within the market. For example, a closer look at central bank balance sheets unveils the liquidity-generating segments that contribute to the overall financial health of the economy. The multiplier effect, influenced by collateral availability and bond market volatility, underscores the reasons behind the resilience of the stock market. With central banks expanding balance sheets and liquidity multipliers, the global liquidity surge becomes a driving force behind market strength. We are seeing a surge in Central banks easing.

The full-length financial report includes the bull case and more and is available to purchase for only £8 at labyrinthcapital.co.uk

An important measure to monitor is looking directly at the liquidity within the banking system. We can use two metrics here, one being the Central Bank balance sheet, the generating parts. Secondly, you want to analyse the extent to which the liquidity can be leveraged throughout the system. This leveraging can come through collateral, which is the backing for loans and also the multiplier that the liquidity has. This is directly related to the degree of volatility in the bond market, the bedrock of the world economy. Many would have assumed that the QT is decreasing the FED balance sheet but this actually is not the case. Central Banks have been expanding their balance sheets forcing global liquidity higher which is another large reason as to why the stock market and crypto have soared.

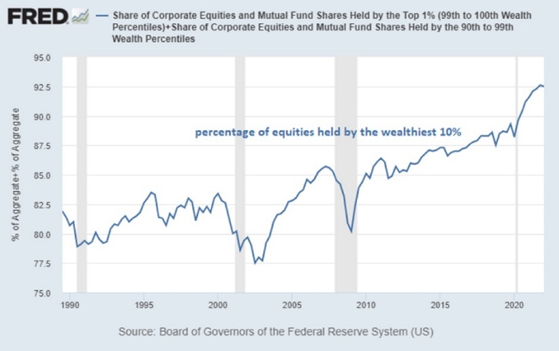

While substantial funds were and are being injected into the economy, it’s crucial to examine where the money is going. The windfall primarily benefited the top quintile of earners and high-net-worth individuals who then actively participated in spending, channelling the funds directly into the U.S. economy. Furthermore, it’s now recorded that 92.5% of equities are held by the top 10% of wealthiest Americans, which is a record-high concentration.

We believe stocks will experience some pain, whether that’s down to higher unemployment, market turmoil ect which will push the FED to likely fold on their plans very quickly.

We believe equally that a lower market expectation will be positive for bonds in 2024. We also have the buyback scheme which we cannot forget about. The only problem with the bond market is it is currently moving very fast and is a big reason for stocks rallying. If we simply look back to when the 30Y was at 1.5%, NAS had an earnings yield of 5.5%. So the difference between locking money with the government vs buying stocks was vast.

Now in October, when rates went to 5%, the earnings yield on NAS was 4.5%. So when we think of changes in institutions they’ll likely be long stocks, but relative to bonds they can also lock in great returns. There could be a heavy shift from equities to bonds which is why you will want to be watching the bond market very closely. Think about it, institutions buying high yield will hit 8% basically with a return on fixed income compared to stocks, and if the economy slides the way of the bears this will likely see portfolios roll into bonds, which will surprise markets. Something to watch.

Currently, there is no denying that stocks are deeply overbought and the reality is, that everyone expected a recession in 2023. The overwhelming consensus was that higher rates would hurt tech stocks but they instead did the opposite. Therefore, as the blow-off top commences we must consider that equal weight will rebalance and sell the Mag 7 after owning it. The institutions when it comes to the new year, will balance the books and take the gains as they summarise their portfolios and trim the index.

Our targets for SPX this year are the following:

H: $4830 — $5000

L: $4500

Our targets for NAS are the following:

H: $17,000

L: $15,600

Crypto:

The crypto market has been pretty hectic since the stock market rallied. One thing you can be certain of is that as soon as Powell initiated the first pivot, dumb money would certainly return, and that it did. Valuations for DeFi startups and seed rounds are nearing that of 2021 and we believe the crypto market is going to be a lucrative business up until the end of Q1 at least. The proponents to consider with crypto is that it runs off the basics of supply and demand. A pure FOMO-driven asset class especially when approaching mid-small caps. The only time crypto makes a downturn and assets bleed will be when Bitcoin melts up. We anticipate this to be around the ETF news drops (which could genuinely be any date in Q1). We expect this to be the event that takes out significant buyside, breaching possibly low 50s before a consequent meltdown. Our targets from 2023 have not changed and for now, we are simply long BTC, XRP, and the assets on our website (labyrinthcapital.co.uk) until liquidity looks to dry up, RRP is drained and the ETF has been announced.

New targets for BTC are as follows:

HL 50.1k

L: 43.6k, 40.1k, 36.6k, 34k, 30k, 24k, 22.5k (breach)

The utility run will happen eventually but for the time being. Market exuberance overrides everything else. Once the BlackRock ETF is approved, BTC can be manipulated and market makers now have a way around the 21m cap on BTC. The eventual push throughout 2024 we can expect is more talk on CBDC where all money is simply 1s and 0s on one ledger held at the central bank.

Conclusion:

To conclude this long format report, we can take away a lot of important factors, indicators, and markets to watch for the upcoming year. Our thesis is evident, we play the market on an intraday basis, longing equities till the reverse repo is drained.

We must still understand that the fiscal situation is not good long-term at all. Around 5% of GDP is towards the MIC. 25% of the GDP is government spending. 7 stocks keep the market at all-time highs. 60% of individuals do not even have $1k in the bank. Rents are pushing through the roof, insurance has gone up 20% this year, both auto and home. All of this, with most jobs paying 25/hr in the US.

It seems hard to make a solid case for equities to drop when looking at the charts, but at the same time, few are worried about a recession, one could argue we have more optimism than ever, all whilst internationally, major parts of the global economies are actually in a recession already. Germany, China, and France are all there, whilst the US showed an incredibly high GDP print, does it make any sustainable sense? We can also look at consumer spending, with companies like Home Depot forecasting lower sales by almost 4%.

One thing that is clear is that the FED has broken the dial on speculative activity pushing it to an ATH since 2008. There has been no true capitulation really and truly. We have seen more euphoria than anything and more optimism than ever. Stocks usually perform well going into a recession so is this what we are seeing? What we must do as investors and traders, is begin to play the ranges more effectively, and coincide this with the bond market as well as be ready for the very real risks the steep incline in real rates will cause as they ripple through the economy.

We hope you found this report useful.

See our social links below:

The full-length financial report includes the bull case and more and is available to purchase for only £8 at labyrinthcapital.co.uk

Sources for graphs:

– US Federal Reserve

– QI Research

– Zero Hedge

– Bloomberg

– Cross Border Capital

![]()

Financial Market Outlook for 2024 was originally published in The Dark Side on Medium, where people are continuing the conversation by highlighting and responding to this story.