Bitcoin treasury firms have entered a Darwinian phase as equity premiums collapse, leverage turns risky, and survival depends on liquidity.

Bitcoin treasury firms have moved into a so-called “Darwinian phase” after equity premiums collapsed across the board.

This trend has changed how these companies grow, borrow and survive. Once easy gains disappeared, risk rose fast. As of writing, Bitcoin treasury firms now face a strict test of balance sheets and strategy.

Bitcoin Treasury Firms Enter Darwinian Phase

Bitcoin treasury firms built their model on a simple idea. Most of them started out with their stock trading above the value of their Bitcoin holdings. That gap allowed them to issue new shares and buy more Bitcoin, and this worked well while prices climbed.

That cycle has now reversed. Bitcoin fell from near $126,000 in October to lows near $80,000. Liquidity dropped, risk appetite weakened and on October 10, a major deleveraging event wiped out large futures positions.

Market depth fell and issuance stopped working as a growth tool.

Galaxy Research described this period as a Darwinian phase. So far, DAT survival now depends on discipline and liquidity.

Bitcoin Treasury Firms See Stocks Flip to Discounts

Bitcoin treasury firms once traded at strong premiums, which created a powerful flywheel of growth. Now, most of these stocks trade at discounts to the Bitcoin they hold.

Companies like Metaplanet and Nakamoto show this clearly. Both companies bought large amounts of Bitcoin near market highs. As of writing, their average entry price sits above $107,000.

Now with Bitcoin well below that level, unrealised losses keep rising.

NAKA stock dropped more than 98% from its peak, and that level of decline matches wipeouts seen in risky token markets.

This event hit harder because Bitcoin itself fell only about 30%, while Bitcoin treasury firms declined much more.

Why the Bitcoin Treasury Firms Model Broke

Bitcoin treasury firms operate like liquidity derivatives. The model depends on stock trading above net asset value, and when that premium holds, the company can issue shares and buy more Bitcoin without hurting existing owners.

Once stock falls below asset value, issuance becomes harmful. Each new share reduces the Bitcoin per share and growth turns into dilution.

Lower Bitcoin price triggered a lower net asset value and equity premiums compressed across the board. Issuance stopped helping, and the loop flipped.

Galaxy Research warned about this pattern months before it happened. And as of writing, the prediction has proved itself correct.

Related Reading: Strategy’s Bitcoin Buys Have Slowed Down Amid Bear Market Jitters

Drawdowns Reveal the Depth of the Problem

Drawdowns across major Bitcoin treasury firms currently show clear stress. Companies like Strategy, Metaplanet, Semler Scientific and Nakamoto all suffered large declines.

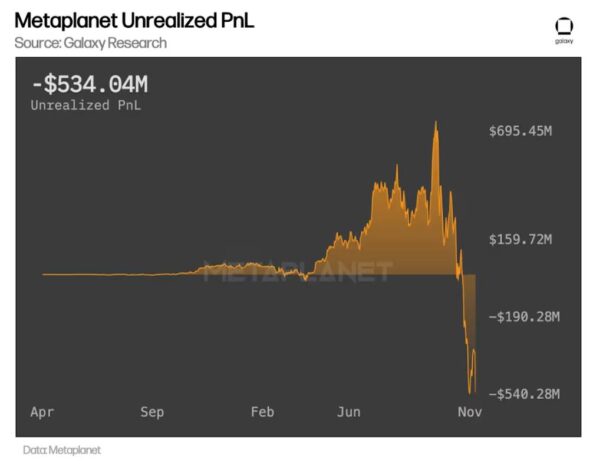

Metaplanet once showed more than $600 million in unrealized gains, but that number has swung to around $530 million in unrealised losses.

In all, Bitcoin treasury firms no longer represent pure upside trades. Instead, they now behave more like complex instruments and each move depends on how and when managers acted.

Investors are now studying balance sheets more closely. Liquidity buffers attract attention, while debt levels raise caution.

This being said, the Darwinian phase will not end quickly. Soft market conditions could last months, and only companies that planned ahead will stay steady.