The S&P 500 has climbed 82% in three years even as the Federal Reserve (Fed) reduced its balance sheet by 27%.

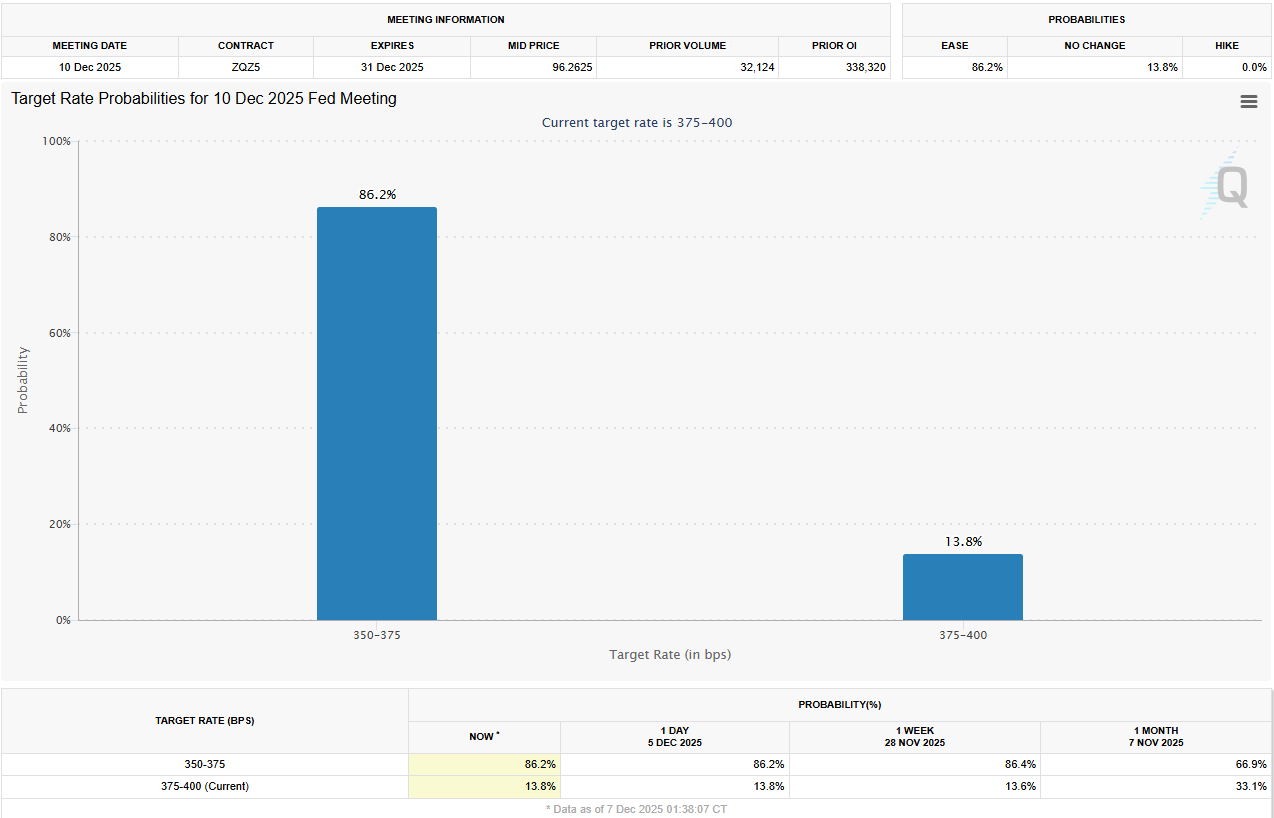

Markets anticipate a 86% chance of a 25 basis point rate cut this week. Nonetheless, economic stress and talk of Fed leadership changes could make policy directions less clear.

Market Performance Surpasses Traditional Liquidity Theories

The equity rally during a period of quantitative tightening has challenged long-standing market beliefs.

Sponsored

Sponsored

Data shared by Charlie Bilello shows the S&P 500 up 82% while Fed assets fell by nearly a quarter.

This separation suggests that factors beyond central bank policies now influence investor confidence. Analysts highlight alternative liquidity sources fueling the rally:

- Fiscal deficits,

- Strong corporate buybacks,

- Foreign capital inflows, and

- Steady bank reserves offset quantitative tightening.

EndGame Macro explains that markets react to expectations for future policy, not only the current balance sheet levels.

However, gains are concentrated in a handful of mega-cap technology companies. As a result, headline market performance disguises sector weaknesses tied to core economic fundamentals.

Psychological liquidity is also significant. Markets respond to anticipated policy changes, not just current conditions. This forward-looking mindset allows equities to rise even when the Fed holds a tightening stance.

Sponsored

Sponsored

Economic Strains Obscured by Stock Gains

Strong stock performance masks deeper economic stress. Corporate bankruptcies are nearing 15-year highs as borrowing costs rise. At the same time, consumer delinquencies on credit cards, auto loans, and student debt are increasing.

Commercial real estate are being impacted by declining property values and harder refinancing terms. These pressures are not reflected in top equity indices, since smaller companies and vulnerable sectors are underrepresented. The link between index performance and wider economic health is now much weaker.

This split suggests that equity markets primarily reflect large firms’ strength. Companies with solid balance sheets and limited consumer exposure tend to perform well, while others dependent on credit or discretionary spending face headwinds.

This economic divide complicates the Federal Reserve’s task. While major stock indexes suggest easy financial conditions, underlying data reveals tightening pressures affecting many areas of the economy.

Fed’s Reputation Pressured as Rate Cut Nears

Many investors and analysts are now questioning the Fed’s direction and effectiveness. James Thorne described it as bloated and behind the curve, urging less reliance on Fed commentary for market signals.

Sponsored

Sponsored

Treasury Secretary Scott Bessent shared pointed criticism in a recent discussion.

“The Fed is turning into a universal basic income for PhD economists. I don’t know what they do. They’re never right … If air traffic controllers did this, no one would get in an airplane,” a user reported, citing Bessent.

These perspectives show rising doubts about the Fed’s ability to forecast economic turns and act quickly. Critics argue that policymakers tend to lag behind markets, fueling uncertainty.

Still, the market expects a 25-basis-point cut this week on Wednesday.

Leadership Uncertainty and Risks for Inflation

Changing leadership at the Federal Reserve adds volatility to policy forecasts. Kevin Hassett leads as the likely replacement for Jerome Powell. Known for his dovish stance, Hassett may bring a looser policy that could raise inflation expectations.

Sponsored

Sponsored

This prospect has moved bond markets. The 10-year Treasury yield has risen as investors weigh whether easier monetary policy under new leadership will push inflation higher. Beyond near-term cuts, markets also price in a broader tone of accommodation.

Investors expect two additional 25-basis-point rate cuts in 2026, likely in March and June. If Hassett becomes Fed chair as early as February, Powell’s remaining term could see him sidelined.

This transition makes Fed policy guidance less predictable as markets focus on the coming change in leadership.

This uncertainty arises while the Fed tries to manage modest inflation above target and a resilient economy under tighter financial conditions. Mistakes in policy or timing could easily rekindle inflation or cause avoidable economic deterioration.

Historical trends provide some context. Charlie Bilello notes that bull markets usually outlast bears by five times, emphasizing the value of compounding returns over market timing.

The ongoing rally could persist, but concentrated gains, economic stress, and doubts about the Fed’s approach make it unclear if markets can remain this resilient as monetary policy evolves.