A widening gap has emerged between the Federal Reserve and financial markets over the trajectory of US interest rates in 2026. While the Fed signals caution on further cuts, markets are betting on two to three reductions this year.

At the heart of this disconnect lies an uncomfortable paradox: President Donald Trump’s push for lower rates may be undermined by the very inflation that threatens his political survival.

Markets Are Betting on Rate Cuts by Mid-Year

According to prediction market platform Polymarket, the probability of a rate cut at the January Federal Open Market Committee (FOMC) meeting stands at just 12%. Most participants expect rates to remain unchanged this month.

But the picture shifts dramatically over a longer horizon. The probability of a rate cut by April rises to 81%, and by June it reaches 94%. For the full year, a two-cut scenario commands the highest probability at 24%, followed by three cuts (20%) and four cuts (17%). Combined, the likelihood of two or more cuts exceeds 87%.

Sponsored

Sponsored

The CME FedWatch tool, which reflects expectations embedded in interest rate futures, paints a similar picture. The probability of a January hold stands at 82.8%, closely matching Polymarket. The likelihood of at least one cut by June is 82.8%, while the probability of two to three cuts by year-end reaches 94.8%.

The market consensus is clear: hold in January, begin cutting in the first half, and deliver two to three reductions by December.

Fed Hawks Signal No Rush

Inside the Fed, however, a different narrative is taking shape. On January 4, Philadelphia Fed President Anna Paulson indicated that further rate cuts may not be appropriate until “later in the year.”

Paulson, who holds a voting seat on the 2026 FOMC, stated that “some modest further adjustments to the funds rate would likely be appropriate later in the year” — but only if inflation moderates, the labor market stabilizes, and growth settles around 2%. She described the current policy stance as “still a little restrictive,” suggesting it continues to work toward lowering inflation pressures.

Her remarks stand in stark contrast to market expectations of a first-half rate cut. The message from the Fed’s hawkish camp is clear: don’t expect action anytime soon.

December FOMC: A Divided Committee

The December FOMC meeting revealed just how fractured the Fed has become.

The committee cut rates by 25 basis points, bringing the target range to 3.5-3.75%. But the vote split 9-3, a wider margin than the previous 10-2 decision. Two members, Schmid and Goolsbee, preferred to hold rates steady. On the other end, Miran — widely viewed as aligned with the Trump administration — pushed for a 50-basis-point cut.

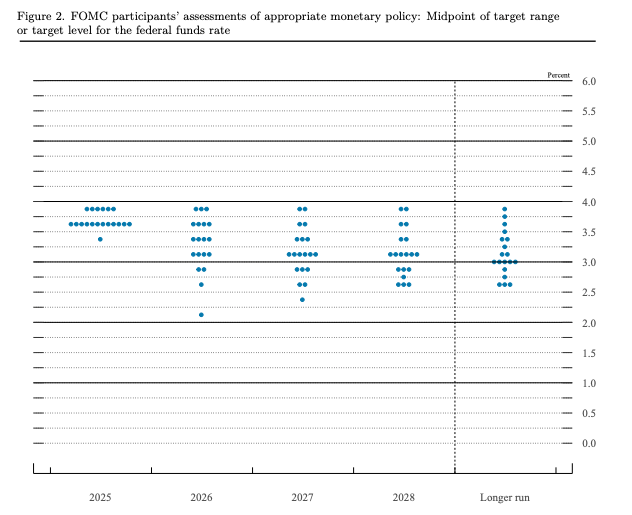

or target level for the federal funds rate. Source: Fed

Sponsored

Sponsored

The dot plot told an even more revealing story. While the median projection pointed to just one cut in 2026, the distribution was extensive. Seven officials projected no cuts at all, while eight saw two or more reductions. The most dovish projection suggested rates could fall as low as 2.125%.

The Fed’s official guidance says one cut. Markets are pricing in two. Why the persistent gap?

Why Markets Are Betting on the Doves: The Trump Factor

The primary reason markets refuse to accept the Fed’s hawkish guidance is President Donald Trump.

Since returning to the office, Trump has consistently pressured the Fed for lower rates. The December FOMC vote — where a Trump-aligned official pushed for aggressive easing — exemplifies this dynamic.

More importantly, Fed Chair Jerome Powell’s term expires in 2026. The power to nominate his successor rests with the President. Market participants widely expect Trump to appoint someone more sympathetic to his preference for looser monetary policy.

Structural factors reinforce this view. The Fed has historically pivoted to rate cuts when the labor market weakens. FOMC divisions are deepening. And there are concerns that tariff policies could slow economic growth, adding pressure for monetary easing.

The market’s bet is straightforward: Trump’s pressure, combined with a potential economic slowdown, will eventually force the Fed’s hand.

Sponsored

Sponsored

The Midterm Paradox: Inflation Is Trump’s Achilles’ Heel

Here lies the central irony. For Trump to effectively pressure the Fed, he needs political capital. But that capital is eroding — because of inflation.

Recent polling shows Trump’s approval rating on economic policy has fallen to 36%. In a PBS/NPR/Marist survey, 57% of respondents disapproved of his economic management. A CBS/YouGov poll found that 50% of Americans say their financial situation has worsened under Trump’s policies.

The culprit is high prices. According to Bureau of Labor Statistics data, ground beef prices have surged 48% since July 2020, while a McDonald’s Big Mac meal has risen from $7.29 in 2019 to over $9.29 in 2024. Egg prices are even more volatile, jumping approximately 170% between December 2019 and December 2024. The term “affordability” has become the dominant economic concern. In the NPR/PBS News/Marist poll, 70% of Americans said the cost of living in their area is “not affordable” for the average family, up sharply from 45% in June.

This discontent is already showing up at the ballot box. In last November’s New York City mayoral race, Democratic state assemblyman Zohran Mamdani won on a platform of making the city more affordable. Democratic candidates also captured governorships in Virginia and New Jersey by emphasizing cost-of-living relief.

With midterm elections approaching in November, over 30 Republican House members have already announced they won’t seek re-election. Political analysts increasingly predict a Republican defeat and a potential lame-duck scenario for Trump.

Three Scenarios, No Easy Path

The intersection of monetary policy and electoral politics produces three possible scenarios for 2026 — none of which give Trump everything he wants.

Scenario 1: Inflation stays elevated. Trump faces political risks, potentially losing the midterms and entering lame-duck status. But high inflation also means the Fed has no justification to cut rates. Trump’s weakened position further diminishes his ability to pressure the central bank.

Scenario 2: The economy cools sharply. Trump faces an even worse political blow as voters punish him for a weakening economy. However, the Fed gains a clear rationale for rate cuts to support growth.

Sponsored

Sponsored

Scenario 3: Soft landing with moderating inflation. Trump’s political standing may recover as economic anxieties ease. But with the economy performing well, the Fed has little reason to cut rates.

In none of these scenarios does Trump achieve both political strength and lower interest rates. The two goals are fundamentally at odds.

The Data That Will Decide Everything

Upcoming economic releases will serve as the decisive variables shaping both Fed policy and Trump’s political fate.

Consumer Price Index (CPI): A decline would strengthen the case for rate cuts and provide Trump with political relief. A rise would constrain the Fed and intensify voter backlash against the administration.

Producer Price Index (PPI): As a leading indicator of consumer prices, a falling PPI would signal future CPI moderation. Rising PPI could indicate that tariff-driven price pressures are materializing.

Employment data (NFP, unemployment rate): Weakening labor markets would increase pressure on the Fed to cut — but would also damage Trump’s economic record. Stable employment would give the Fed cover to maintain its cautious stance.

Conclusion

The Fed is signaling one rate cut in 2026. Hawks like Paulson suggest even that may not come until the second half. Yet markets continue to price in two to three cuts, betting that Trump’s pressure and the Powell succession will ultimately push the Fed toward easing.

But here’s the paradox: persistent inflation erodes Trump’s political standing, which in turn weakens his leverage over the Fed. The very conditions that make rate cuts politically desirable for Trump also make them economically unjustifiable — or strip him of the power to demand them.

“It’s the prices, stupid” applies to Trump, to the Fed, and to market participants alike. In the end, inflation and employment data will simultaneously determine the path of US interest rates and the outcome of November’s midterm elections. Trump may want both political survival and lower rates, but the economy is unlikely to grant him that luxury.