Why Stablecoin Regulation Is Speeding Up — From D.C. to Hong Kong

This week, the U.S. Senate and the Hong Kong Legislative Council nearly simultaneously took major steps in stablecoin regulation: the former overwhelmingly passed a procedural motion on the GENIUS Act, clearing the way for the first federal stablecoin legislation in the United States; the latter passed the third reading of the “Stablecoin Ordinance Bill,” making Hong Kong the first jurisdiction in Asia-Pacific to establish a stablecoin licensing regime. The synchronicity of Eastern and Western legislative progress is no coincidence — it reflects a broader contest for influence over the future financial order.

Stablecoin Transaction Volume Could Surpass $100 Trillion Annually by 2030

According to preliminary statistics from OKG Research, the global stablecoin market capitalization is approaching $250 billion, having grown more than 22-fold over the past five years. Since the beginning of 2025, on-chain transaction volume has surpassed $3.7 trillion and is projected to reach nearly $10 trillion for the year. Stablecoins such as USDT and USDC are now widely used in emerging markets for trading and remittances, with usage volumes surpassing traditional payment systems in some regions. What was once considered a fringe asset has become a core node in global payment networks and a tool for sovereign competition. The near-simultaneous legislative efforts in the U.S. and Hong Kong signify that the global stablecoin market has entered a period of accelerated regulatory alignment.

Based on this, OKG Research — drawing on Standard Chartered’s earlier projection model and factoring in the pace of current regulatory signals and institutional sentiment — has developed the following estimates under an optimistic scenario where global regulatory frameworks are adopted and stablecoins gain widespread use by individuals and institutions:

- Global stablecoin supply could reach $3 trillion by around 2030.

- Monthly on-chain transaction volume could reach $9 trillion.

- Annual transaction volume may exceed $100 trillion.

This would position stablecoins not only alongside traditional electronic payment systems but as foundational assets in global clearing networks. In terms of asset scale, stablecoins would become the “fourth major base currency asset” after sovereign bonds, cash, and bank deposits — serving as a key medium for digital payments and asset circulation.

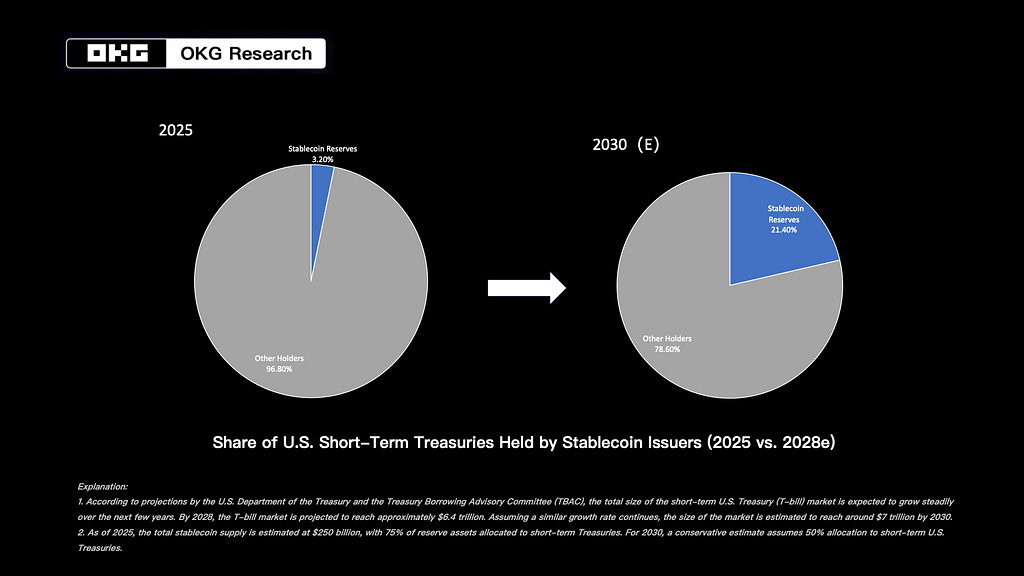

More notably, the reserve structure of stablecoins under such expansion could have macroeconomic implications. As OKG Research previously reported, current stablecoin holdings account for roughly 3% of maturing short-term U.S. Treasury bills — ranking 19th among overseas holders.

Considering the GENIUS Act mandates that 100% of reserves be held in highly liquid U.S. dollar assets — with short-term Treasuries as a primary component (over 80% of current USDT/USDC reserves are linked to short-term Treasuries) — a conservative 50% allocation of a $3 trillion market would create at least $1.5 trillion in structural demand for short-term U.S. debt. This volume is close to the current holdings of sovereign investors like China or Japan, suggesting stablecoins could soon become the U.S. Treasury’s largest “invisible creditor.”

Comparing the U.S. and Hong Kong Stablecoin Regulatory Frameworks: Divergences Amid Consensus

While the U.S. and Hong Kong differ in legislative paths and technical details, they share consensus on core principles: fiat-pegging, full reserve backing, and licensed issuance.

The GENIUS Act applies to “payment stablecoins,” defined as tokens pegged to legal tender (e.g., USD), redeemable at 1:1 value, and prohibited from offering interest — ensuring they are not treated as securities or investment vehicles. Hong Kong, while also requiring full backing, does not restrict interest payments or asset structures in the current draft, leaving room for future innovations in a dollar-dominated stablecoin landscape.

Both jurisdictions mandate full reserve backing with high-liquidity assets, though the GENIUS Act defines acceptable reserve assets (T-bills, cash, repos) and mandates monthly audits. Hong Kong similarly requires audits and segregated custody but leaves asset types more open.

In terms of regulatory structure, the GENIUS Act adopts a federal-state dual framework, offering three issuance pathways: (1) through a licensed bank or its subsidiary (regulated by the Fed, FDIC, etc.), (2) directly licensed by the OCC for non-bank entities, or (3) through qualified state licensing regimes. Hong Kong’s Monetary Authority (HKMA) handles all licensing and mandates that any issuer — whether based in Hong Kong or abroad — must apply for a license if issuing HKD-pegged stablecoins or marketing services to Hong Kong residents.

Regarding foreign issuers, the GENIUS Act prohibits unlicensed overseas stablecoins from circulating in the U.S., allowing the Treasury to designate “non-compliant stablecoins” and instructing digital asset service providers to block their flow. Hong Kong focuses primarily on HKD-pegged stablecoins and remains more open to foreign currencies.

These structural differences reflect divergent policy goals. The U.S. seeks to preserve dollar hegemony and address fiscal needs by extending dollar dominance onto the blockchain. In contrast, Hong Kong aims to attract global Web3 projects while maintaining local financial stability, crafting a “regulated sandbox” in Asia-Pacific that balances control with openness and interoperability.

How Will Stablecoin Regulation Reshape the Web3 Ecosystem?

The real significance of stablecoin regulation lies in providing foundational infrastructure for large-scale Web3 adoption.

In DeFi, while USDT and USDC are already key settlement assets, their uncertain legal status has hindered institutional participation. The enactment of frameworks like the GENIUS Act would allow compliant issuers to become the settlement backbone of “compliant DeFi,” incorporating KYC, AML, and asset recognition modules. Decentralized finance would evolve into “auditable on-chain financial networks.”

In Web3 payments, regulation will remove gray zones between assets and payment scenarios, transforming stablecoins from transaction intermediaries into payment channels. Since Visa announced over $225 million in stablecoin settlements, many fintech firms have integrated stablecoins into merchant flows. Web3 wallets use stablecoins as default assets for microtransactions like top-ups, tips, and subscriptions. The transition from “crypto-native transfers” to “enterprise-grade financial APIs” depends on regulatory clarity.

At a deeper level, this reshapes global clearing architecture. Stablecoins — pegged 1:1 to fiat currencies — bridge fiat and on-chain assets while bypassing traditional banking rails, enabling peer-to-peer clearing. This could allow stablecoins to replace traditional banks with cross-border payments, trade finance, and RWA (real-world asset) payouts.

Historically, discussions on Web3 adoption focused too much on tech and UX, neglecting the legitimacy of core financial assets. Compliant stablecoins offer the missing piece: legally recognized, programmable, fiat-linked digital assets that can be used across DeFi and NFT ecosystems.

In essence, stablecoins are not auxiliary to Web3 — they are a primary catalyst. With regulatory support, they will underpin everything from RWA tokenization to payroll, cross-border settlements, and Web3 payment rails — becoming the foundational infrastructure for global on-chain economies.

![]()

Why Stablecoin Regulation Is Speeding Up — From D.C. to Hong Kong was originally published in The Capital on Medium, where people are continuing the conversation by highlighting and responding to this story.