The CLARITY Act is moving toward the Senate floor with a promise crypto has spent years asking for: a clearer federal map for digital asset markets.

The under-covered risk is that the map runs through the CFTC, making CFTC crypto regulation a capacity test for spot-market oversight after its payroll workforce fell by more than one-fifth.

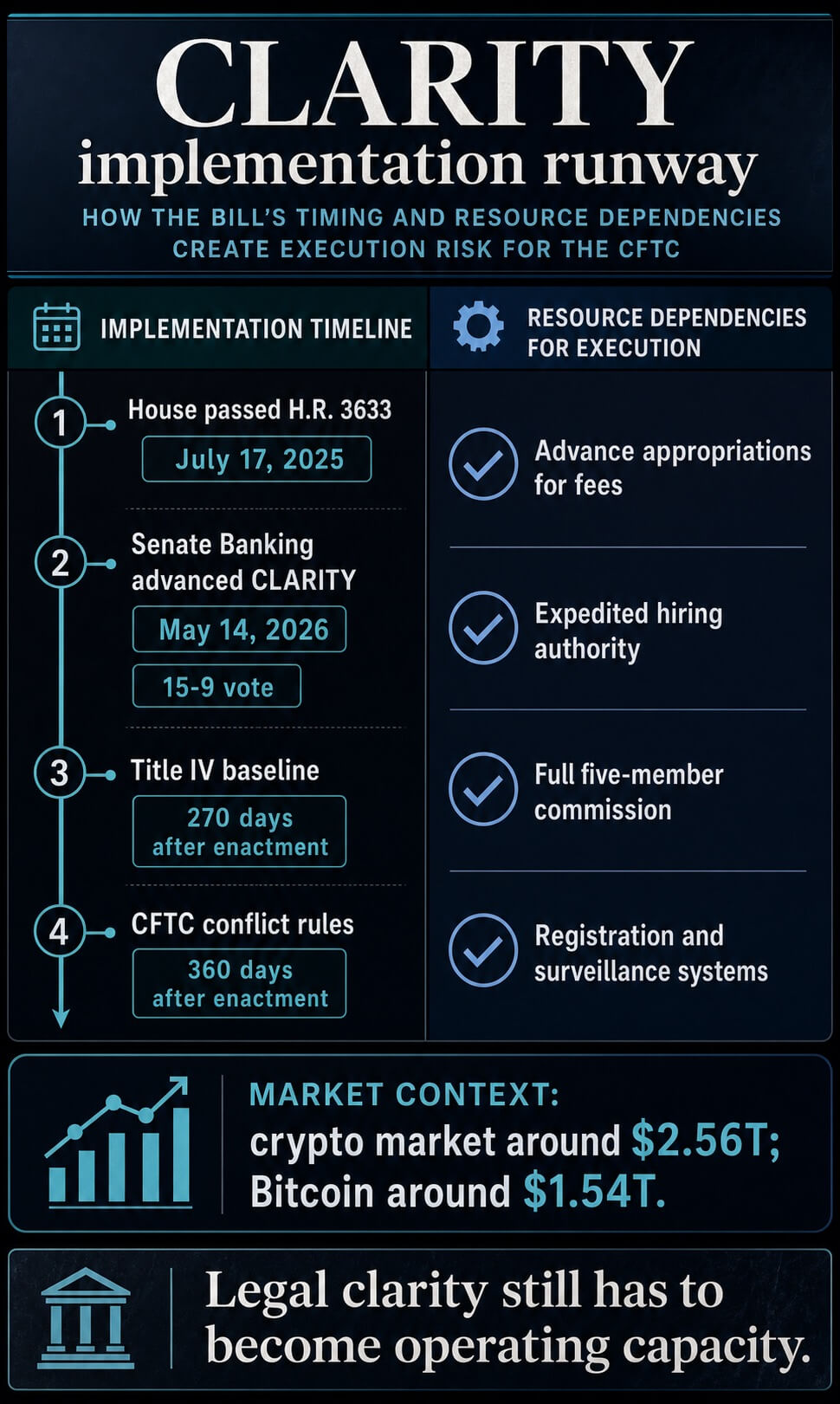

The Senate Banking Committee advanced H.R. 3633 on May 14 by a 15-9 vote, putting the Digital Asset Market Clarity Act of 2025 closer to floor consideration after the House passed the bill in July 2025.

Votes and signing timelines have dominated the crypto market structure bill debate. The implementation test is capacity.

The bill would make the Commodity Futures Trading Commission the main federal overseer for a large slice of crypto spot-market activity. It requires the CFTC to generally regulate digital commodity transactions, including digital commodity exchanges, brokers, and dealers, with trade monitoring, recordkeeping, and customer-asset commingling restrictions.

That is a broad operating mandate for an agency whose own watchdog has already flagged digital-asset legislation and human-capital management as top FY2026 challenges.

Expanded digital-asset jurisdiction may require new registrant categories, rulemakings, cooperative regulatory efforts, qualified staff, institutional expertise, additional data systems and analytics, and management of added budget resources, according to the CFTC Office of Inspector General.

However, the same OIG report said CFTC payroll full-time equivalents fell from roughly 708 at the end of FY2024 to about 556 at the end of FY2025, an approximate 21.5% reduction.

The mandate is larger than the vote

The bill would shift jurisdiction from the SEC to the CFTC while forcing an operating buildout.

A new spot-market regime means exchanges and intermediaries would need rules for registration, trade surveillance, recordkeeping, conflicts, customer assets, conduct standards, and anti-fraud enforcement.

Some of that work can be adapted from futures-market supervision. Much of it would still have to be written, staffed, reviewed, and updated for crypto market plumbing.

The House-passed text sets a 270-day effective date for Title IV unless otherwise provided and directs the CFTC to issue conflict-of-interest rules within 360 days of enactment.

Those timelines may change as Senate negotiations proceed, but the House baseline shows the gap between statutory clarity and agency execution. Congress can assign the job in one bill; the regulator still has to hire, write rules, register firms, build systems, and supervise markets.

That is where the capacity issue becomes more than a budget footnote.

| CLARITY Act would require | Current capacity signal | Implementation consequence |

|---|---|---|

| New digital commodity registrant categories | CFTC OIG says expanded jurisdiction may require new registrant categories and qualified staff | Crypto firms cannot operate under a clear regime until registration rules and review capacity exist |

| Rulemakings and conflict rules | House text gives a 360-day deadline for CFTC conflict-of-interest rules | The promise of clarity depends on detailed rules beyond statutory labels |

| Market surveillance and enforcement | CFTC budget tables show enforcement FTEs at 140 in FY2025 actual, 105 in FY2026 enacted, and 108 requested for FY2027 | Anti-fraud and anti-manipulation authority needs investigators, data, and exam capacity behind it |

| Commission-level rulemaking depth | CFTC’s current commissioners page lists only Michael S. Selig in the current commissioners section of a five-seat structure | House Agriculture leaders argue major crypto rules are more durable when they come from a fully staffed bipartisan commission |

The numbers also complicate the easy version of the pro-CLARITY Act argument.

CFTC’s FY2027 request seeks $410 million, up from a $365 million FY2026 enacted base for salaries and expenses, and requests 650 FTEs against a 636-FTE FY2026 baseline.

That is a real funding increase, but the requested headcount change is only 14 FTEs over the FY2026 baseline.

That increase sits beside an OIG report describing a far larger operational load and a recent payroll FTE drop of more than one-fifth.

Resource tools still need money

The House-passed bill acknowledges the resource problem. Section 410 would authorize filing fees and annual fees tied to digital commodity regulation and registration, and it would create expedited hiring authority for positions requiring digital commodities or specialized market knowledge.

Those tools still have to become usable resources. The fee authority is tied to amounts provided in advance by appropriations, and the section’s authorities sunset after the fourth fiscal year beginning after enactment.

In plain English, the CLARITY Act contains mechanisms to help the CFTC scale, but they still depend on Congress making the money available and on the agency converting authority into people, systems, and supervision.

That distinction is crucial because the bill’s market effect depends on the second step.

Practical clarity starts when rules are final, registration pathways are open, compliance expectations are known, and enforcement lines are visible enough that market participants can price legal risk.

Senate Agriculture leaders have already recognized the issue.

A Boozman-Booker market-structure draft release said the approach would create a new CFTC funding stream, while Sen. John Boozman said the agency would need staffing and resources in place on day one to handle expanded authority.

The CFTC digital-assets agenda is also advancing while Congress negotiates.

Chairman Michael S. Selig told the House Agriculture Committee in April that the agency was working on areas including crypto guidance, tokenized collateral, prediction markets, payment stablecoin capital treatment, enforcement, and market surveillance.

That agenda may help the agency prepare, but it also shows that the CLARITY Act would land on top of an already active policy and supervision workload.

The enforcement line is especially important for retail users. The CLARITY Act would give tokens and venues a cleaner legal home while also promising federal guardrails for spot markets.

The FY2027 request would leave enforcement FTEs below the FY2025 actual level even as spot-market jurisdiction is expected to expand, meaning Congress may have created a cleaner rulebook faster than it created the staff needed to police it.

Commission depth is part of capacity

Staffing is only one side of implementation. Governance bandwidth is the other.

The CFTC’s commissioners page says the agency consists of five commissioners and, as of May 19, lists Selig as chairman in its current commissioners section.

Selig was sworn in on Dec. 22, 2025. The current page display should be treated as institutional-depth evidence rather than a legal conclusion about what the agency can or cannot do.

House Agriculture leaders made that point explicit in a May 15 letter to President Donald Trump.

The letter said legislation expanding the CFTC’s mandate to bring spot digital commodity transactions under federal oversight would require significant rulemaking. It also said a full five-member commission would help produce better and more durable rules.

The broader crypto market is measured in trillions, which gives the implementation risk real scale while keeping price reaction outside the record.

CryptoSlate market pages show the total crypto market capitalization around $2.56 trillion, with Bitcoin alone around $1.54 trillion.

Commission depth also intersects with political risk.

Sen. Angela Alsobrooks, who voted to advance the bill in committee, said that vote did not guarantee support on the Senate floor and flagged unresolved financial-crime and ethics issues.

Senate Banking minority staff separately argued the draft leaves illicit-finance and DeFi vulnerabilities.

Those critiques could reshape final text, and any unresolved conduct risks Congress leaves in the statute can become supervisory problems for the agency asked to run the regime.

Timing makes the capacity risk more concrete.

Galaxy Digital’s early-August signing scenario, recently reported by CryptoSlate, would turn the CFTC’s staffing, funding, and commissioner depth from a policy concern into a countdown if Congress keeps pace.

The CLARITY Act already gives the CFTC some tools for the job. The House text includes funding and hiring mechanisms, Senate Agriculture has tied market-structure authority to resources, and CFTC leadership is already building a digital-asset agenda.

Execution is the pressure point.

A market-structure bill paired with weak appropriations, thin commission depth, or a short hiring runway could leave crypto with more statutory clarity than operational clarity.

Firms would know which regulator controls the next phase, then still wait for the rules, registrations, reviews, and enforcement posture that make the regime usable.

The next test for the CLARITY Act reaches beyond Senate passage or a presidential signature.