Has Donald Trump been net positive for Bitcoin? It is an uncomfortable question for many Bitcoin supporters, including me.

My political criticisms of Trump are substantial and longstanding. They extend well beyond policy disagreements into questions about rhetoric, institutional conduct, and the broader political culture surrounding his presidency.

None of that disappears because Bitcoin performed well during parts of his administration or because parts of the industry now view him as an ally. Still, the question matters because Bitcoin increasingly sits inside state policy, capital markets, and geopolitical competition.

Once that happened, separating political preference from analytical judgment became harder. The reason the question deserves a serious answer is simple: no modern U.S. president has moved Bitcoin closer to formal government recognition than Trump.

That does not automatically make him “good for Bitcoin” in a complete sense. Price appreciation alone is insufficient. Campaign rhetoric is insufficient. Political branding is insufficient.

The real test is whether Bitcoin has become more institutionally durable, more legally defensible, and more difficult for future governments to marginalize.

On that narrower question, the evidence is stronger than many critics like me want to admit.

Trump’s Bitcoin legacy rests on whether political recognition became durable institutional protection.

So, to dig into it, Donald Trump has been positive for Bitcoin in one important and provable way: he moved it closer to the center of U.S. government policy than any prior president.

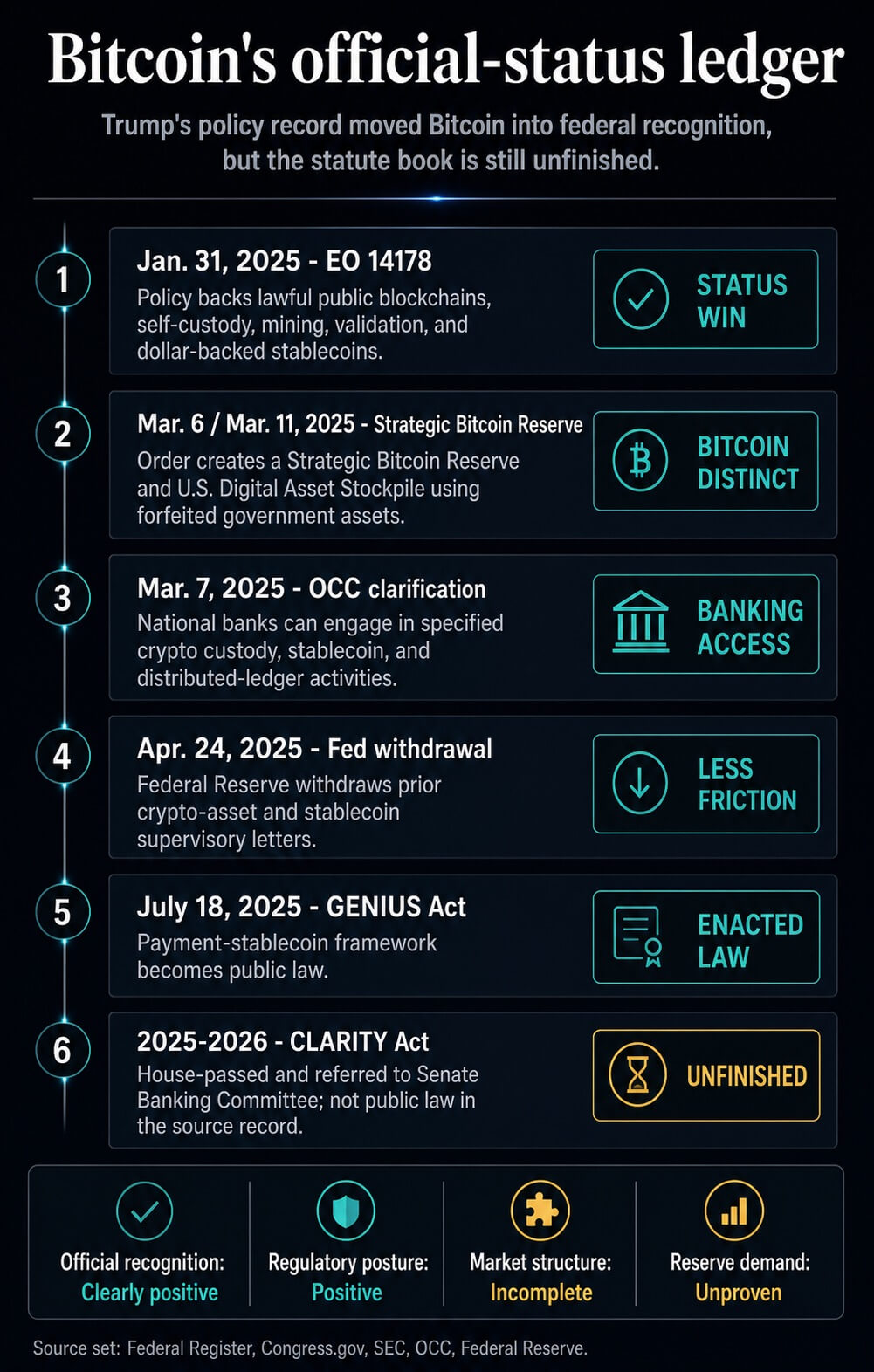

The clearest evidence comes from the federal record: an executive order endorsing lawful use of public blockchains, self-custody, mining, and validation, followed by a separate order creating a Strategic Bitcoin Reserve and a U.S. Digital Asset Stockpile.

That shift changed Bitcoin’s political ceiling. The U.S. government stopped treating it only as an asset to be policed, taxed, or liquidated, and began describing it as something the state could hold as a reserve asset.

For investors and institutions, that lowers the perceived risk of a federal ban or of hostile banking policy returning unchanged.

The broader record is less sweeping. Price action is mixed. Regulation has improved, while the law on Bitcoin itself remains incomplete.

Yet public trust remains weak. The blockchain has yet to show a simple adoption boom. Trump-linked crypto businesses have also created a separate reputation problem that Bitcoin supporters cannot dismiss by saying the protocol is apolitical.

The answer is therefore ledger-specific. Trump’s Bitcoin record is strongest where government recognition, institutional access, and political permission are the test.

It is weaker where the test is price durability, public confidence, durable statute, or organic base-layer use.

| Ledger | What the evidence shows | Verdict |

|---|---|---|

| Price | Up from election day, down from inauguration and the reserve order, and roughly 37% below the October 2025 high. | Mixed |

| Ideological status | Public blockchains, mining, self-custody, and a Bitcoin reserve are now explicit U.S. policy positions. | Clearly positive |

| Regulation | Stablecoin law and agency posture improved, while market-structure law is unfinished. | Positive but incomplete |

| Public reputation | Polling still shows low ownership, high risk perception, and weak confidence. | Weak |

| On-chain use | Transactions rose at the selected endpoints, while addresses and fees fail to confirm broad base-layer demand. | Unproven |

Price and policy tell different stories

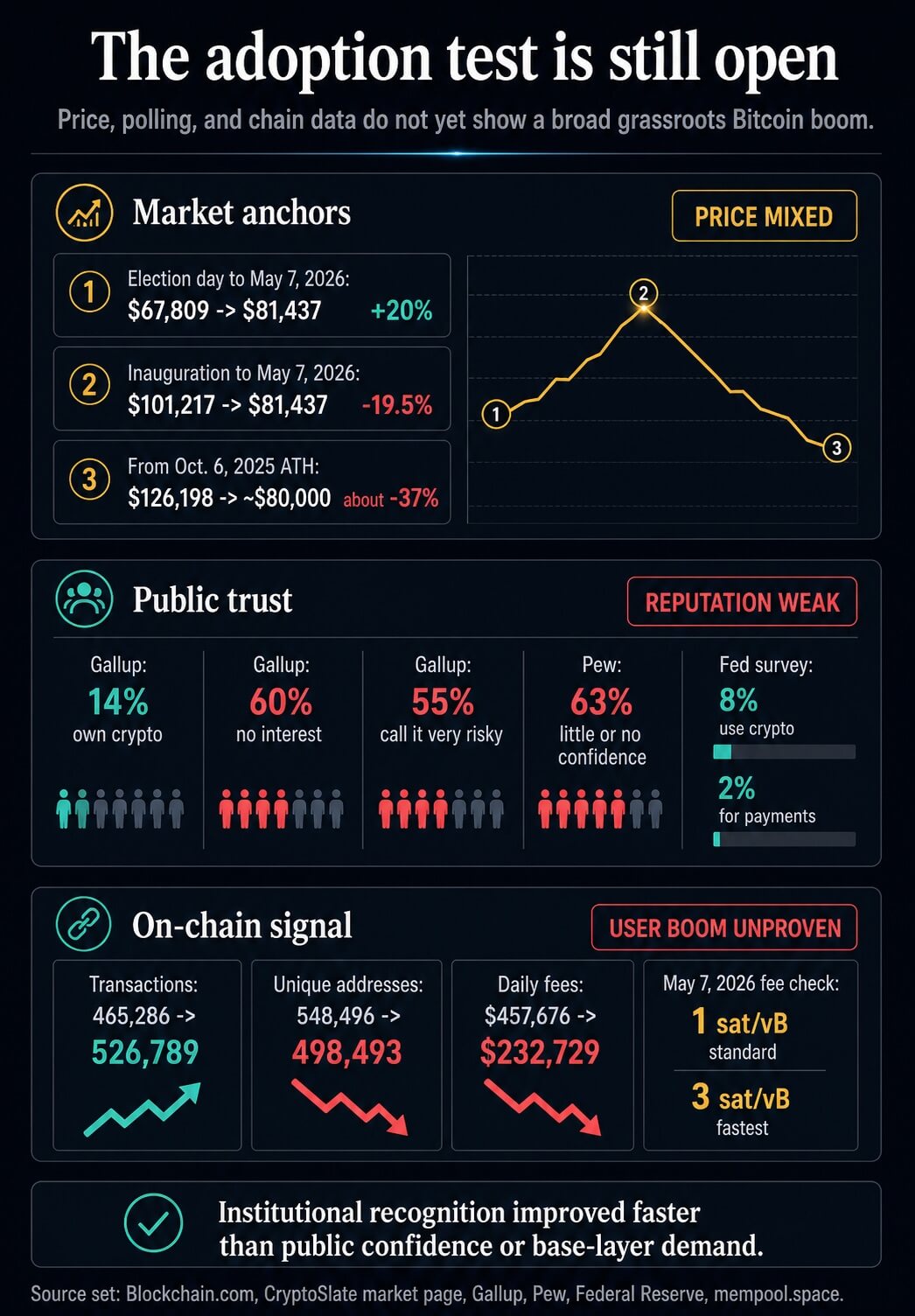

The price case depends on where the measurement begins. Bitcoin sat near $67,800 on Nov. 5, 2024, and about $80,700 on May 10, 2026.

From that election-day anchor, Bitcoin is up by roughly 20%. That supports the view that Trump’s victory, policy signals, and the broader post-halving cycle coincided with a meaningful market repricing.

Other politically relevant anchors give a weaker read. Bitcoin was about $101,200 on Jan. 20, 2025, Trump’s inauguration day.

It was around $90,600 on March 6, 2025, when the Strategic Bitcoin Reserve order was signed. Measured from those points, the market is lower.

CryptoSlate’s Bitcoin page also places BTC just above $80,000 this weekend, roughly 37% below its Oct. 6, 2025, all-time high of $126,198.

The honest price verdict is mixed. Trump-era policy helped create a friendlier backdrop, and Bitcoin did reach a new high during that period.

Current price action still falls short of proving a durable Trump premium. It shows a rally that later gave back a large share of its gains, leaving the market positive from election day and negative from inauguration.

Policy gives Trump a stronger claim. Executive Order 14178 made support for lawful digital-asset use an explicit U.S. policy, including public blockchain networks, self-custody, mining, validating, and dollar-backed stablecoins.

Executive Order 14233 went further by establishing the Strategic Bitcoin Reserve, giving Bitcoin distinct treatment from other digital assets in the federal stockpile.

That is a real status change. It turns Bitcoin from something the U.S. government mostly seized, sold, or argued about into something the government says it will retain as a reserve asset.

It also creates a political fact that future administrations would have to reverse openly if they wanted to return to a more hostile posture.

The limit is equally important. The reserve order capitalizes the reserve with forfeited government BTC and permits only budget-neutral acquisition strategies that impose no incremental taxpayer cost.

The reserve’s immediate force is recognition, custody, and potential restraint from sell pressure. New sovereign demand would require acquisition records that are currently lacking.

Regulation follows the same pattern. The GENIUS Act was enacted as federal law and created a payment-stablecoin framework.

The SEC’s SAB 122, the OCC’s March 2025 clarification, and the Federal Reserve’s withdrawal of prior crypto guidance all made the banking and custody environment less hostile.

Those are material changes. The central Bitcoin market-structure fight remains unfinished.

The CLARITY Act has passed the House and been referred to the Senate Banking Committee, but has not yet become public law.

In practical terms, Trump can claim a real shift in executive and agency posture, plus one major stablecoin statute. He cannot yet claim that Bitcoin’s full federal market-structure problem has been solved by enacted law.

Public reputation did not follow the official endorsement

The weakest part of the pro-Trump case is public reputation. Gallup found in June 2025 that 14% of U.S. adults owned cryptocurrency, 60% had no interest in buying it, and 55% considered it very risky.

Pew’s October 2024 baseline was similarly hostile: 63% of Americans had little or no confidence that crypto is reliable and safe, while 17% had ever invested, traded, or used it.

Those surveys are imperfect measures of Trump’s second-term effect. Pew predates the term, and Gallup predates some later Trump-linked crypto controversies.

Even with that timing caveat, they show the starting terrain and first-year public response. Bitcoin and crypto have yet to become trusted mass-market institutions because the president embraced them.

The Federal Reserve’s household survey adds another check. In 2024, 8% of adults used crypto for any purpose, while only 2% used it to buy something or make a payment.

That points to an asset still understood mainly as a speculative or investment product, rather than an everyday monetary tool.

This is where the reputation ledger cuts against the official-status ledger. A reserve order can change how fund managers, bank compliance teams, and public-market investors price political risk.

It has much less power over households shaped by exchange failures, scams, meme-coin cycles, and partisan suspicion. Official recognition can lower institutional fear while leaving popular distrust largely intact.

Trump’s personal and family crypto ties complicate the reputation ledger further. Associated Press reporting on Trump-linked crypto business relationships and CryptoSlate’s coverage of scrutiny around World Liberty Financial support a credible conflict-of-interest concern.

The sourced record supports reputation and ethics risk, plus allegation context. It falls short of proving criminal wrongdoing or showing that Bitcoin’s protocol has been compromised.

For Bitcoin, that distinction is uncomfortable.

Still, public reputation is built through association as well as technical design. A president can strip Bitcoin of its official status while also making crypto look more self-serving to people who already distrust it.

Chain data leaves the adoption case unproven

On-chain evidence is the other major restraint on the net-positive claim. Blockchain.com data show daily confirmed transactions rising from 465,286 on Nov. 5, 2024, to 526,789 at the end of last week.

That is a positive endpoint comparison. Daily unique addresses fell from 548,496 to 498,493 over the same endpoints, and daily transaction fees fell from about $457,676 to about $232,729.

Those figures need careful handling. Unique addresses are a poor proxy for people, and daily endpoints can be distorted by batching, exchange flows, transaction composition, and non-monetary activity.

Still, they fail to support a clean claim that Trump’s policy shift brought a wave of base-layer users into Bitcoin.

Independent on-chain analysis points in the same direction. Glassnode described a 2025 divergence between elevated BTC prices and quieter network activity, including low fee pressure and dominance by large entities.

Galaxy separately argued that fee pressure had faded after late-2024 Runes and Ordinals activity cooled.

A mempool.space check also showed a quiet point-in-time fee market, with 1 sat/vB recommended for half-hour, hour, economy, and minimum fee targets and 3 sat/vB for fastest confirmation.

That picture is mixed rather than bearish in every sense. Low fees make Bitcoin cheaper to use, and high prices can reflect institutional demand moving through ETFs, custodians, treasuries, and off-chain venues rather than base-layer transaction growth.

It does limit the adoption claim. Trump’s Bitcoin effect looks stronger in official recognition and institutional channels than in everyday blockspace demand.

The sourced record supports a conditional answer. Trump has been positive for Bitcoin’s ideological status and institutional access.

He turned public-blockchain support into executive policy, created a version of a Strategic Bitcoin Reserve, backed a friendlier agency posture, and signed a major stablecoin law that helps crypto market infrastructure.

The rest of the ledger is weaker. Bitcoin’s price is positive from election day and negative from inauguration and reserve-order anchors.

The reserve is real, but with no verified evidence here of an active government accumulation program. Market-structure law remains unfinished. Public trust is still low.

On-chain activity shows no simple grassroots boom. Trump-linked crypto conflicts create a credible reputation drag by association, even without proving criminality.

The most defensible answer is yes, in a limited sense. Trump has been net positive where government recognition, institutional access, and political permission are the main tests.

He has yet to be clearly net positive, where Bitcoin’s broader legitimacy ultimately has to show up: public confidence, durable law, and organic network use.

The next developments that would change the judgment are concrete reserve accounting, any new record of BTC acquisitions, final market-structure legislation, changing public-opinion data, and sustained on-chain demand that cannot be explained primarily by speculation or institutional custody flows.