Strategy’s (formerly MicroStrategy) flagship dividend-paying preferred stock is trading at its weakest level this year, pressuring one of the company’s most important tools for raising capital to buy Bitcoin.

The $10.5 billion variable-rate perpetual preferred stock, which trades under the ticker STRC, closed Tuesday at $91.79.

The settlement marked its third-lowest close since trading began in July 2025 and left the security well below the $100 level that the Michael Saylor-led firm has tried to keep it near.

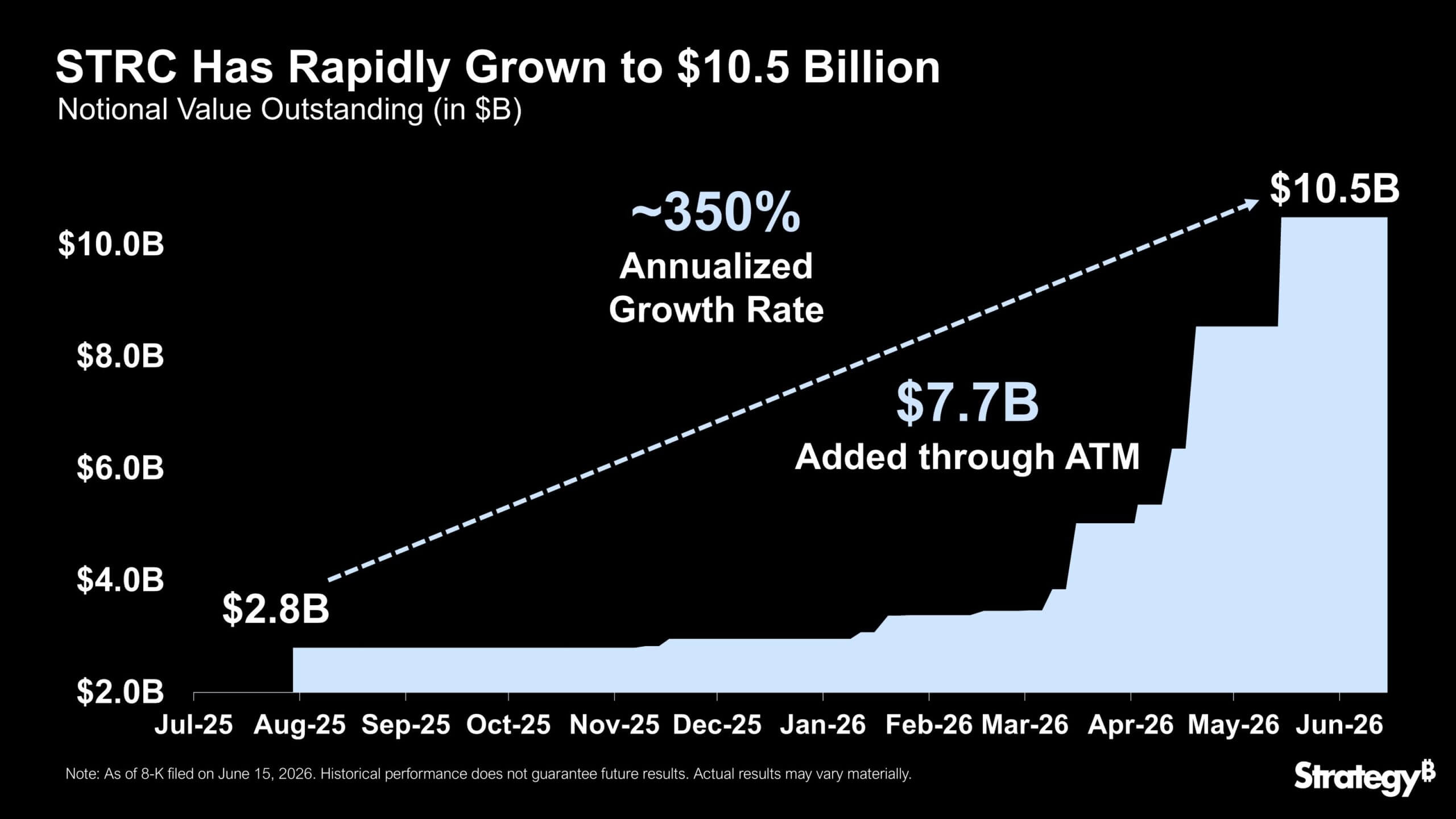

Over the past year, STRC has expanded from $2.8 billion to $10.5 billion, adding $7.7 billion through at-the-market issuance. This made it one of the fastest-growing financial products in history.

So, the decline has turned STRC into a live test of investor appetite for Bitcoin-linked income products. Strategy built the instrument to offer a high dividend while giving the company another way to raise capital.

However, the market is now tacitly demanding a higher yield as Bitcoin pulls back, rival preferred stocks offer more attractive terms, and investors reassess the risks attached to Strategy’s expanding capital structure.

Bitcoin’s pullback reaches the preferred stack

STRC’s weakness shows how quickly Strategy’s income products can start trading under the same pressure as the asset underlying the company’s balance sheet.

During the spring, strong demand and a rising Bitcoin price allowed Strategy to keep the STRC dividend rate unchanged at 11.5%. The stock traded close enough to par that management had little reason to raise the payout.

However, that changed as Bitcoin rolled over and investors began asking for more compensation to hold a preferred stock tied to a company whose value is deeply exposed to the cryptocurrency.

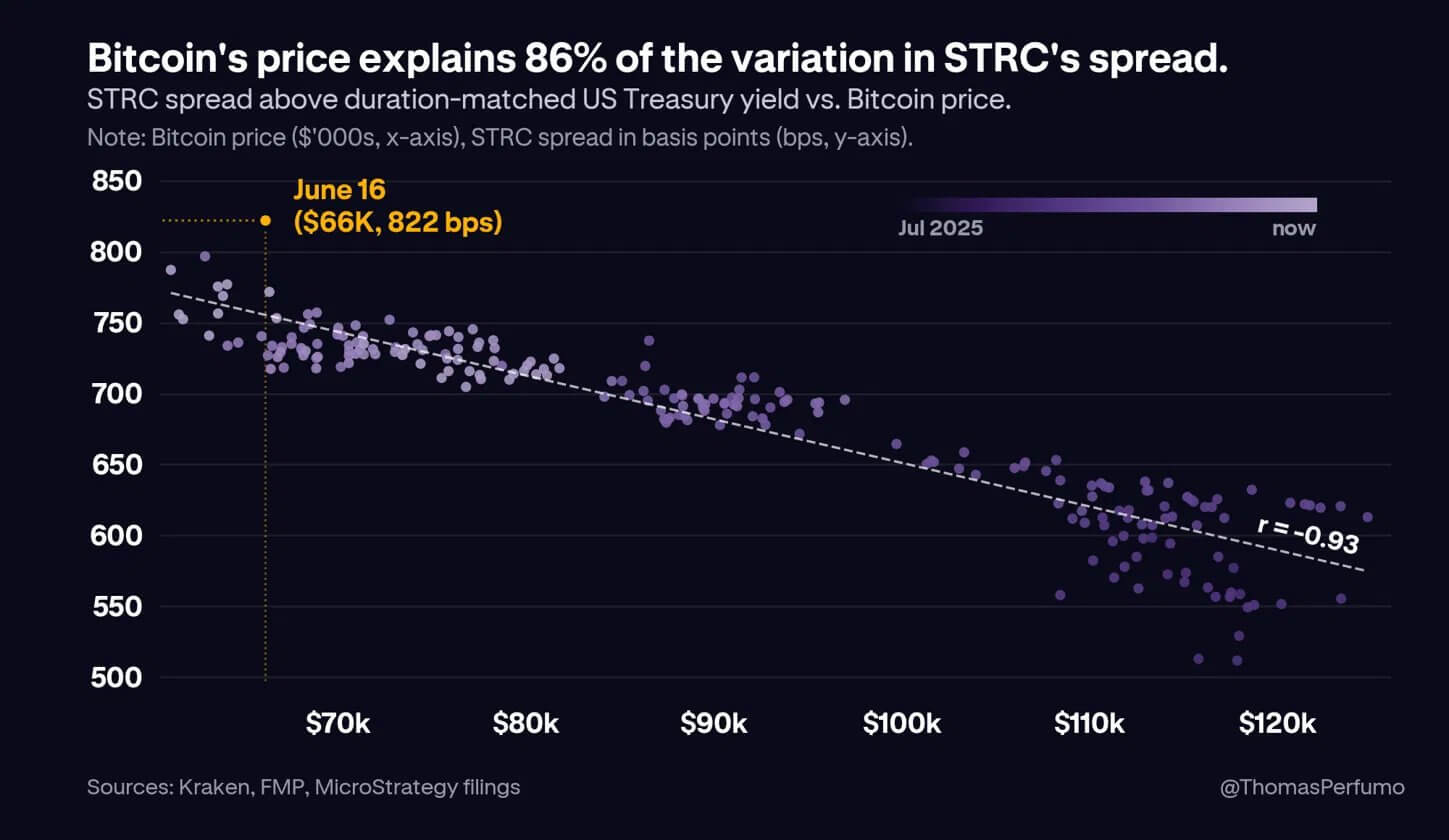

Kraken chief economist Thomas Perfumo said about 86% of the variation in STRC’s yield spread can be explained by moves in Bitcoin’s price. His analysis suggests investors are treating STRC less like a stable preferred stock and more like a credit product whose risk premium moves with Bitcoin.

That relationship is not unique to STRC. Other Strategy preferred securities, including STRK, STRD, and STRF, have also shown pressure.

The difference is that investors expect those instruments to move around. STRC was marketed with a stronger price-stability objective, making its extended discount more difficult for holders to dismiss.

The market math is straightforward. STRC pays an annual dividend of $11.50. At a price near $92, investors are earning about 12.6%.

To bring the stock back toward $100, Strategy would likely need to raise the dividend closer to the yield investors are already demanding. Andre Dragosh, Bitwise Europe’s head of research, stated:

“Saylor essentially needs to raise the dividend by slightly more than 1$ to pull STRC to par. Equilibrium dividend is at around 12.6$ right now.”

The soft-peg problem

STRC’s design gives Strategy flexibility, but it does not force the market to value the stock at $100.

The product has a stated amount of $100, and Strategy can adjust the dividend rate to encourage trading near that level. But there is no automatic mechanism requiring buyers to step in at par. That distinction has become central to the current selloff.

Parker White, chief operating officer and chief investment officer at DeFi Development Corp., said the product’s soft $100 anchor may have made it vulnerable to short sellers.

He argues that STRC’s retail-heavy investor base expected the stock to stay close to par, so a move even a few dollars below that level can trigger outsized concern.

According to him, short sellers may be able to exploit that reaction because the cost to borrow STRC is relatively low.

White continued that the outright borrowing cost is about 60 basis points, making the trade cheap to maintain compared with similar products. Strategy’s at-the-market issuance program may also limit upside above $100, reducing the risk that short sellers face if they position against the stock.

The theory gives traders a clear pressure point. If investors treat $100 as a promise rather than a target, every move away from that level can weaken confidence.

That risk is more pronounced because some crypto protocols have been built around STRC or use Strategy-linked securities as part of broader yield strategies. A sustained decline could force some holders to reassess collateral values, liquidity assumptions, and expected returns.

Strive’s SATA raises the comparison

White also noted that STRC’s discount has become more visible because a rival product is holding up better.

Strive’s bitcoin-backed preferred stock, SATA, has continued to trade close to its $100 par value while offering a higher annualized payout of about 13%. It also pays dividends daily, rather than monthly or semi-monthly, giving investors faster cash distribution and making the product more expensive to short.

That structure has strengthened SATA’s appeal among income-focused investors. Daily dividends reduce the pressure that often builds around ex-dividend dates, when holders decide whether to collect the payout or rotate elsewhere.

They also increase the carrying cost for short sellers, who must account for dividend obligations more frequently.

White estimated that SATA’s baseline borrowing cost is about 460 basis points. Including the effect of daily dividend obligations, he said the annualized cost to short SATA rises toward 17.6%, compared with about 60 basis points for STRC.

The comparison puts Strategy in a difficult position. STRC still offers a high stated payout, but the market is showing a preference for both higher yield and faster payments.

Restoring STRC comes with a cost

STRC’s decline has left Strategy with a narrower path to restore confidence in one of its most important funding channels.

White has argued that the company could stabilize the product by raising the dividend to 12%, calling a shareholder vote to move to daily payments, increasing the call price from $101 to at least $110, and rebuilding the cash buffer to $2.5 billion.

According to him, higher dividends and daily payments would make STRC more expensive to short. A higher call price would give the stock more room to trade above $100, increasing the risk for traders betting against it.

Additionally, the larger cash reserve would reduce concerns about dividend coverage and help reassure income-focused investors.

However, each step would carry a significant trade-off that could impact Strategy.

For context, A higher payout could help pull STRC closer to par, but it would also increase Strategy’s recurring cash burden. Daily dividends may improve market confidence, but would require another structural change. A larger reserve could strengthen the credit profile, but may slow the pace of new Bitcoin purchases.

The larger challenge is the investor base. STRC still appears to be owned heavily by Bitcoin-native buyers, who compare the preferred stock with Bitcoin itself.

When Bitcoin falls, those investors can either collect income from STRC or rotate back into spot Bitcoin at lower prices. That competition forces Strategy to offer a higher return than traditional fixed-income buyers might require.

A broader investor base could reduce that pressure. For money-market, preferred-stock, and fixed-income investors, an 11.5% cash dividend remains large.

However, attracting that capital may require stronger proof that STRC can hold its range even during Bitcoin drawdowns.